Warren Buffett: Closet Dividend Investor - Seeking Alpha

In addition to that, Berkshire is expected to earn fat dividends from itsinvestments in preferred stocks in General Electric (GE) and Goldman Sachs (GS) as well.

Warren Buffett’s latest annual letter to Berkshire Hathaway (BRK.A) shareholders was published on Feb 26. The major theme of this letter was how to value Berkshire Hathaway as a company. Given the diverse nature of the company’s operations, this is no small task. Another important item that the Oracle of Omaha discussed was the dividend stream that flows to Berkshire on a regular basis.

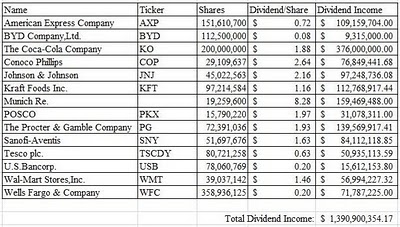

In a previous article I outlined several reasons why Buffett is a dividend investor. While his investment style in the 1950s – 1970s was simply to purchase stocks trading at a discount to their fair values, it evolved into purchasing entire businesses or equity stakes in them. The common characteristic of these businesses was that they had strong competitive advantages, high returns on equity and as a result were generating excess cash flows. Buffett then used these excess cashflows to invest in other businesses, thus further compounding his capital base. Another characteristic common to Buffett’s stock investments is that most of them pay a dividend as evidenced by the largest positions for Berkshire Hathaway (BRK.A), below, click to enlarge:

In addition to that, Berkshire is expected to earn fat dividends from itsinvestments in preferred stocks in General Electric (GE) and Goldman Sachs (GS) as well.

For the foreign based shares listed above I converted the amount of shares Berkshire Held at Dec 31, 2010 to the respective number of ADRs traded on US exchanges. For any currency translations I used the exchange rate as of Dec 31 as well.

Of particular importance are Buffett’s investments in Coca-Cola (KO), Procter & Gamble (PG) and The Washington Post (WPO), which was not listed above.

Buffett’s cost basis in Coca-Cola (KO) is $1.3 billion. At the current distributions rate he is essentially generating a yield on cost of 29%. This means that every three years he gets his initial investment back in the form of dividends alone. The majority of his position in the company was initiated between 1988 and 1989. Check my analysis of Coca-Cola (KO).

In Buffett’s words:

Other companies we hold are likely to increase their dividends as well. Coca-Cola paid us $88 million in 1995, the year after we finished purchasing the stock. Every year since, Coke has increased its dividend. In 2011, we will almost certainly receive $376 million from Coke, up $24 million from last year. Within ten years, I would expect that $376 million to double. By the end of that period, I wouldn’t be surprised to see our share of Coke’s annual earnings exceed 100% of what we paid for the investment. Time is the friend of the wonderful business.

Buffett’s cost basis in Procter & Gamble (PG) is $464 million. He is generating a yield on cost of over 31% for his shareholders on this investment. The original investment in 1989 was made in Gillette preferred stock, which was converted into common stock in 1991. In 2005 Procter & Gamble (PG) acquired Gillette, which is how Buffett ended up with Procter & Gamble (PG) stock in the process. Check my analysisof Procter & Gamble.

Buffett’s basis in Washington Post (WPO) is $6.15/share. With a current dividend of $9.40, Berkshire’s yield on cost is 153%. The Oracle of Omaha began acquiring stock in the prominent newspaper group in 1973.

The lesson to be learned from these investments is to purchase great businesses at fair prices. These businesses should have a strong competitive advantage, pricing power and generate excess returns without requiring a lot of capital to grow.

Full Disclosure: Long PG, KO, JNJ, KFT, WMT

No comments:

Post a Comment