Technology stocks have historically been thought of as growth stocks. In truth, the majority of technology stocks have been quite cyclical. But most importantly, technology has not been thought of as a dividend growth sector, until recently that is. As the technology sector has matured, from the start up, new industry, fast growth phase of their business evolutions, the nature of their business models and attitude toward shareholders has matured and evolved as well. Many technology stocks, including some of the biggest and best-known have instituted dividend policies in recent years. Consequently, this industry, once thought of as a pure growth industry, is rapidly morphing into a dividend growth story.

Since technology stocks behaving as dividend growth stocks is such a new phenomenon, you won't find any of them on David Fish's "Dividend Champions" list. However, many are beginning to show up on his lists of "Contenders and Challengers." Consequently, many traditional dividend growth seekers may not be comfortable with mining the various technology sectors for dividend growth candidates. However, that may be a mistake, especially for those investors seeking above-average dividend growth and/or above-average total return. With technology becoming an integral, normal, and to a greater extent, an essential part of the business landscape, the forward-thinking dividend seeker may want to consider turbo charging their dividend growth portfolios with some high-tech.

Screening for Value

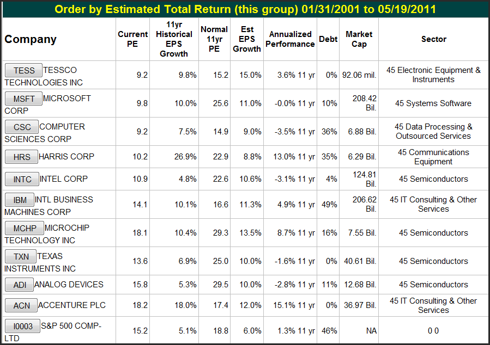

Therefore, we ran a screen utilizing our research tool's screener, looking exclusively for dividend paying information technology stocks. After screening our database of over 16,000 symbols, including ADRs, we discovered over 50 information-technology companies that paid a dividend yield of at least 1%. Interestingly, these companies ranged in size from very small cap companies with less than $100 million in total capitalization, to industry behemoths like Microsoft (MSFT) and IBM (IBM). Then we ran an individual graph on each of the initial 50 candidates in order to whittle the list down to our top 10. It's important to note that our top 10 candidates are offered as candidates for a more extensive research process. However, to be worthy of a more exhaustive research process, each of the companies had to currently possess several important attributes. First, was a focus on profitability. Each candidate had to be profitable since calendar year 2001, which was the first year after the infamous "tech bubble." Even more importantly, each candidate had to remain profitable through the great recession of 2008. Then we turned our focus to valuation. Each candidate had to appear reasonably enough valued in order to offer a potential double digit total return over the next five years, based on the consensus analyst estimates for earnings growth. To ensure that the dividend was reasonably well protected, we looked for companies with debt below 50% of total capital, and operating activity cash flows greater than earnings per share.

10 Information-Technology Dividend Growth Stocks

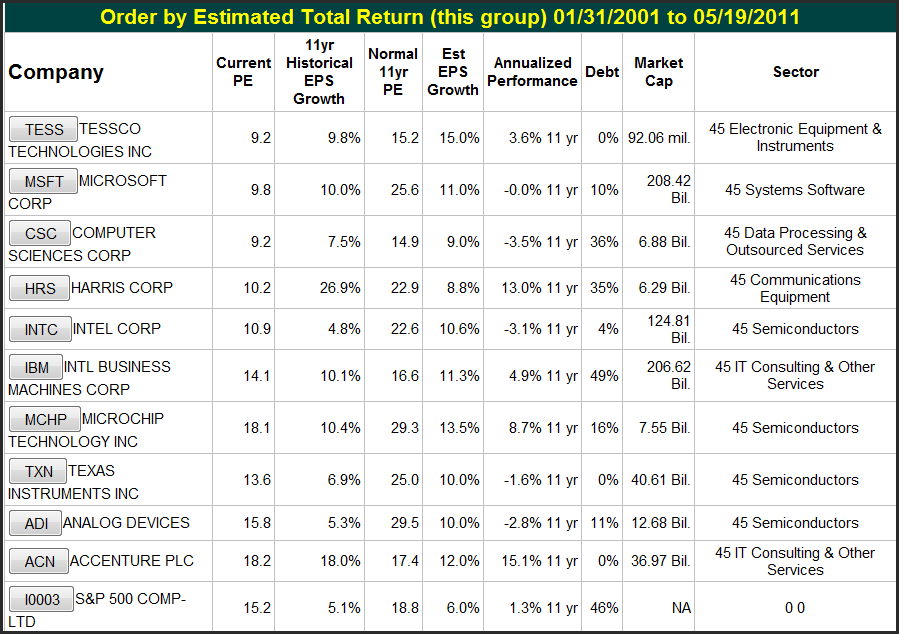

the graph portfolio review table below provides a summary of our 10 choices of information technology companies as potential solid dividend growth stocks. The companies are listed in order of highest five-year estimated annual total return based on consensus estimates to the lowest.

(Click to enlarge)Fundamentals-at-a-Glance

The following looks at each of our candidates through the lens of our three basic graphs; two historical and one forecast. On each company, we provide an earnings and price correlated graph to include its associated performance results, followed by the estimated earnings and return calculator based on consensus analyst estimates. A brief overview of each stock is provided courtesy of each company's standard press release description. Then we provide a short narrative to assist the reader in interpreting each of the presented our graphs.

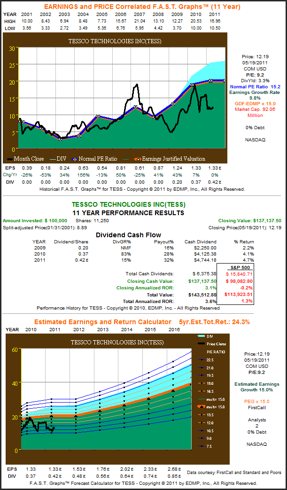

"About TESSCO

TESSCO Technologies, (TESS), is Your Total Source to build, use, and maintain wireless systems. The convergence of wireless and the Internet is revolutionizing the way we live and work. New systems and applications are unlocking human potential at an unprecedented rate. TESSCO is there, thinking in new ways for exceptional outcomes. TESSCO architects and delivers, with innovation, productivity and speed, the product and value chain solutions to organizations responsible for building, operating, and maintaining wireless voice, data and video systems." The graph on Tessco (TESS) show that earnings growth, after falling in 2001 and 2002, has been very strong since calendar year 2003. The company has no debt and they instituted their first dividend in calendar year 2009. As a small cap, there are only two analysts reporting to FirstCall. However, they do estimate earnings growth of 15% over the next five years. This would indicate extreme undervaluation as their current PE ratio is less than 10.

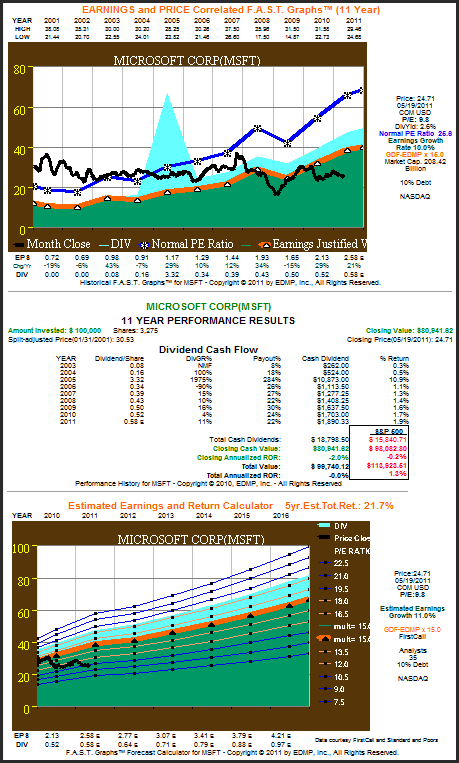

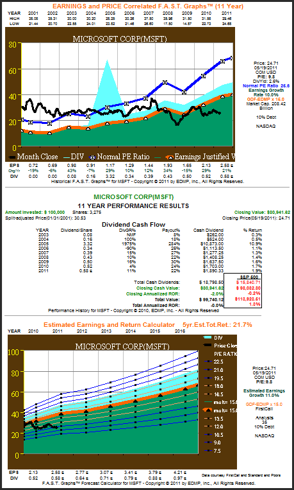

(Click to enlarge)"About Microsoft

Founded in 1975, Microsoft (MSFT) is the worldwide leader in software, services and solutions that help people and businesses realize their full potential." The graph on Microsoft shows that the stock was significantly overvalued in 2001, which led to poor shareholder returns, even though operating results were strong. Note that the company has increased their dividend every year since instituting one in calendar year 2003. The big spike in the light blue shaded area (dividends) indicates the $3.00 special dividend they paid in calendar year 2005. The regular dividend increased from $.32 in calendar year 2005 to $.34 in 2006. Therefore, the indicated -90% drop is not accurate, as it is calculated from the special distribution. Microsoft appears undervalued with a PE ratio of 9.8 and expected consensus five-year earnings growth of 11%.

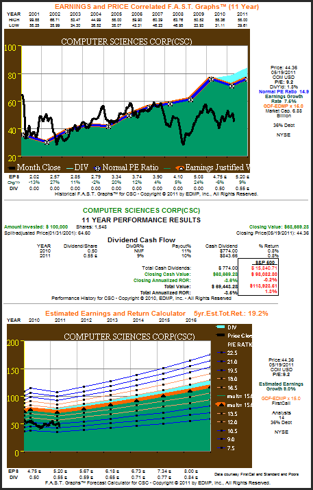

(Click to enlarge)"About CSC

CSC is a global leader in providing technology-enabled solutions and services through three primary lines of business. These include Business Solutions and Services, the Managed Services Sector and the North American Public Sector. CSC's advanced capabilities include system design and integration, information technology and business process outsourcing, applications software development, Web and application hosting, mission support and management consulting."

The graph on Computer Sciences Corp. (CSC) shows fairly steady earnings growth since fiscal year 2002. The company instituted their first dividend in 2010. The consensus of 14 analysts expect five-year earnings growth of 9%. The normal PE ratio for this mid-cap technology company has been approximately equal to the market multiple of 15 times earnings. Therefore, with the current PE ratio below 10, the company appears to be undervalued.

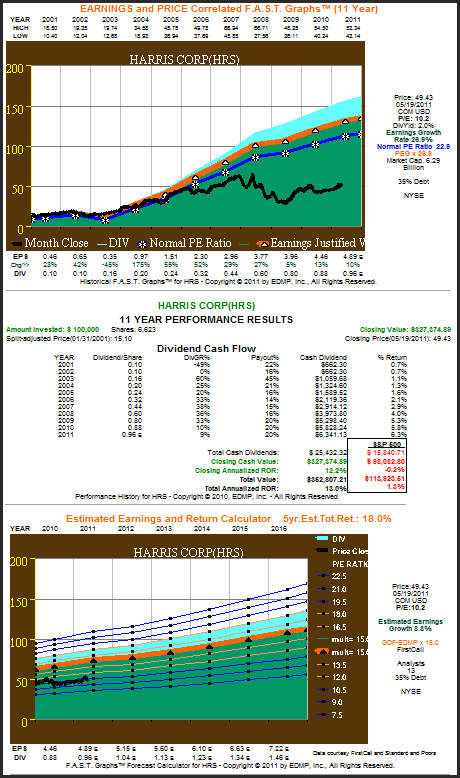

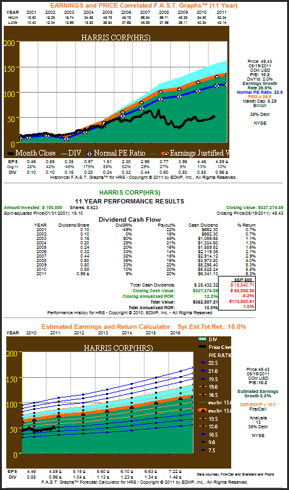

(Click to enlarge)"About Harris Corporation

Harris is an international communications and information technology company serving government and commercial markets in more than 150 countries. Headquartered in Melbourne, Florida, the company has approximately $6 billion of annual revenue and more than 16,000 employees — including nearly 7,000 engineers and scientists."

The graph on Harris Corp. (HRS) shows steady earnings growth since calendar year 2001. Although Harris Corp. has paid a dividend for many years, it's only thanks to its current low valuation that today's entry yield equals 2%. Furthermore, Harris Corp. has increased their dividend every year since 2002. The consensus analyst estimates for five-year earnings growth is approximately 9%. Therefore, the current PE ratio just above 10 times earnings is less than half their historical normal PE ratio.

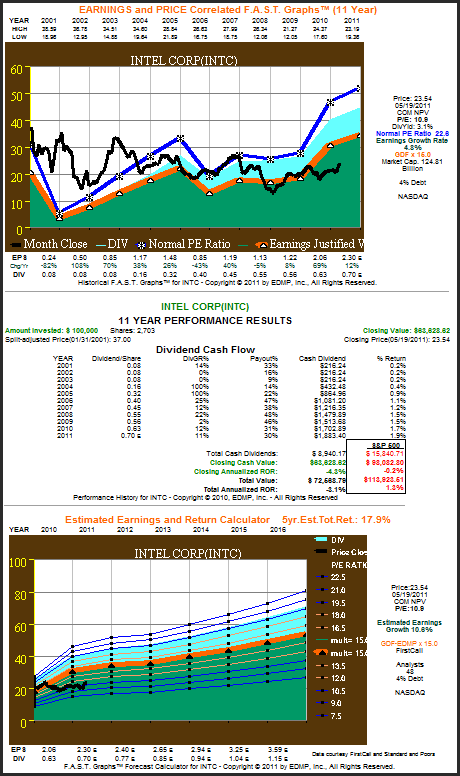

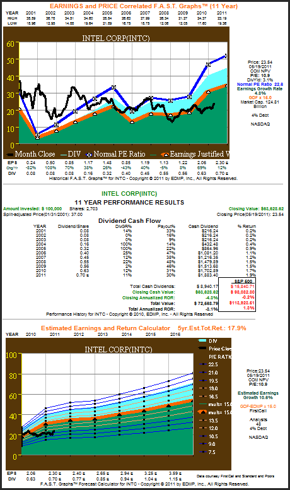

(Click to enlarge)"About Intel

Intel (INTC) is a world leader in computing innovation. The company designs and builds the essential technologies that serve as the foundation for the world's computing devices." the graph shows that Intel was still overvalued after the bursting of the tech bubble in 2000. Also, earnings growth since calendar year 2002 has been reasonably strong. Although Intel has been paying a small dividend for many years, prior to calendar year 2001, their payout ratio was only single digits. However, since that time Intel has been paying out a more normal 30% to 40% of their earnings to shareholders in the form of dividends. With a current PE ratio of 10.9 and a 3.1% current yield, Intel appears very attractively valued today. The consensus five-year earnings estimate of analysts is 10.6%. Intel has only 4% debt, and with operating cash flows higher than earnings, their dividend seems well covered.

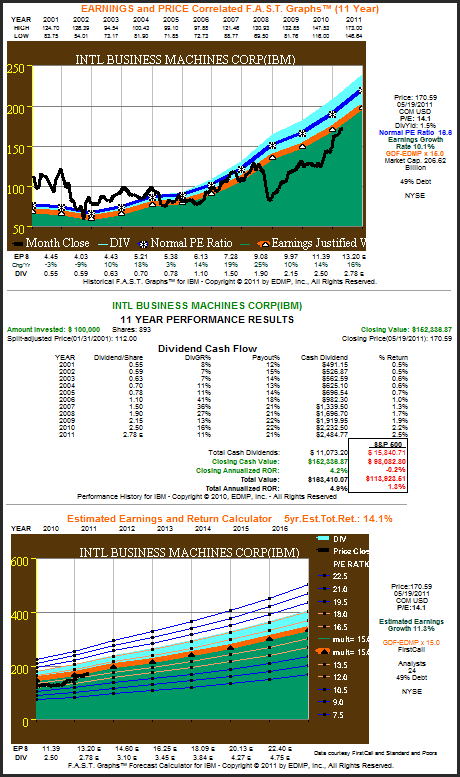

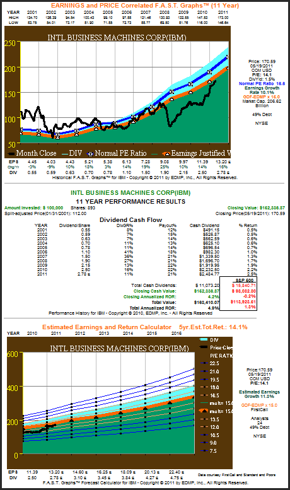

(Click to enlarge)"About IBM

An IBM (IBM) supercomputer broke the petaflop barrier in 2008 and it is one of 100 Icons of Progress or top achievements in IBM's century-long history. Now the focus is on delivering multi-petaflop systems that will eventually lead us to exascale class systems -- a thousand-fold increase." The graph on IBM illustrates a very consistent pattern of earnings growth since calendar year 2003. Prior to 2007, IBM's payout ratio was in the teens, but has more recently expanded to over 20%. With the consensus analysts' five-year earnings growth estimate of 11.3%, IBM appears fairly valued with a current PE ratio of 14.1. With the potential for their payout ratio to continue to increase, there exists a possibility that their dividend can continue to grow faster than earnings.

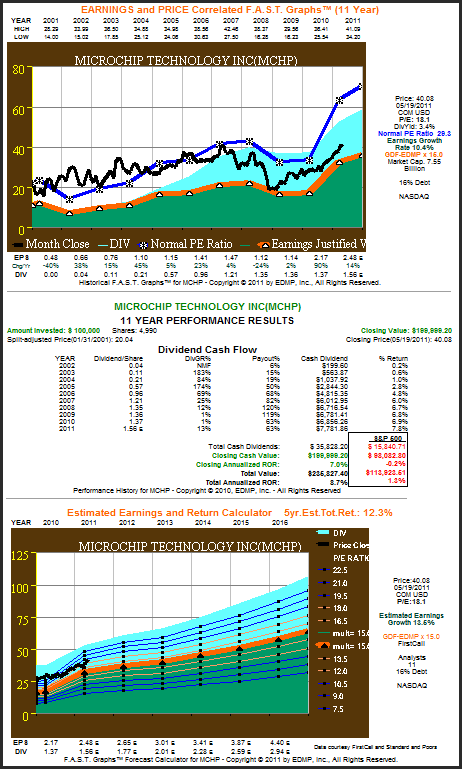

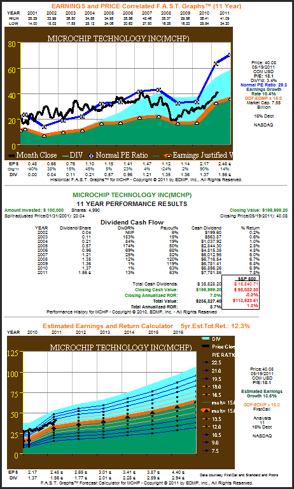

(Click to enlarge)"Microchip Technology Incorporated

Microchip Technology Incorporated is a leading provider of microcontroller, analog and Flash-IP solutions, providing low-risk product development, lower total system cost and faster time to market for thousands of diverse customer applications worldwide. Headquartered in Chandler, Arizona, Microchip offers outstanding technical support along with dependable delivery and quality."

The graph on Microchip Technology Inc. (MCHP) depicts a company with reasonably consistent double-digit earnings growth since calendar year 2002. Although they suffered a modest drop in earnings during the recession of 2008, the company remained strongly profitable. Furthermore, they did raise their dividend that year, albeit ever so slightly. Even though the consensus five-year earnings growth rate is 13.5%, the second highest of the group, their current PE ratio above 18 indicates that the stock may be fully valued. However, the 3.4% dividend yield with the potential to grow at double-digit rates may be attractive to certain income seeking investors.

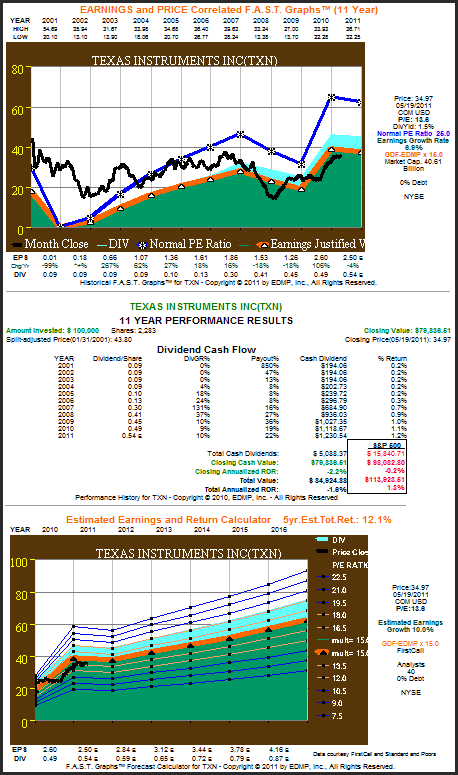

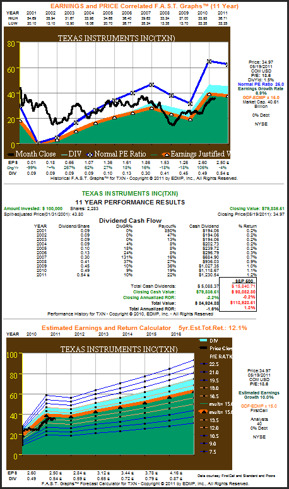

(Click to enlarge)"About Texas Instruments

Texas Instruments semiconductor innovations help 80,000 customers unlock the possibilities of the world as it could be – smarter, safer, greener, healthier and more fun. Our commitment to building a better future is ingrained in everything we do – from the responsible manufacturing of our semiconductors, to caring for our employees, to giving back inside our communities."

The graph on Texas Instruments (TXN) shows another example of a technology company that suffered from overvaluation coming out of technology bubble. However, with the consensus five-year earnings growth rate estimate of 10%, the company appears fairly valued with ratio of 13.6. The graph also illustrates that the company has become more committed to paying dividends since calendar year 2007 when their payout ratio expanded to 16%, and has steadily gone higher ever since.

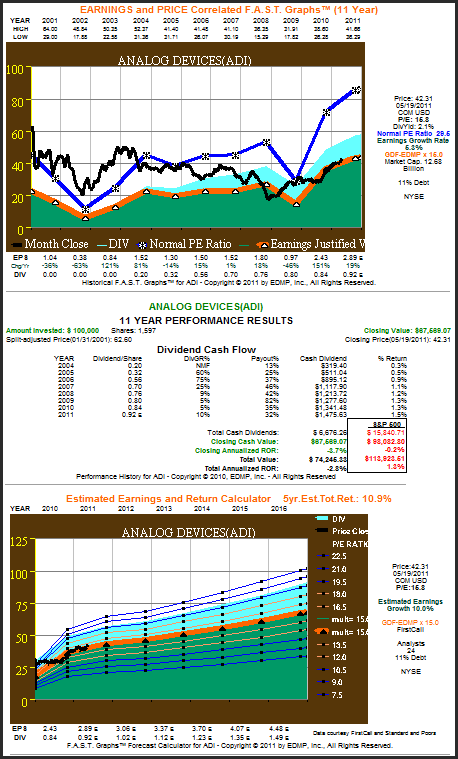

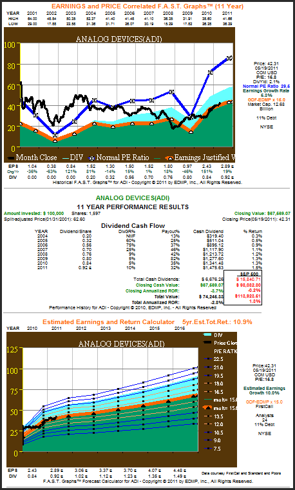

(Click to enlarge)"About Analog Devices

Innovation, performance, and excellence are the cultural pillars on which Analog Devices has built one of the longest standing, highest growth companies within the technology sector. Acknowledged industry-wide as the world leader in data conversion and signal conditioning technology, Analog Devices serves over 60,000 customers, representing virtually all types of electronic equipment. Analog Devices is headquartered in Norwood, Massachusetts, with design and manufacturing facilities throughout the world."

The graph on Analog Devices (ADI) shows that earnings growth has moderated in recent years. The company has instituted their first dividend in calendar year 2004 and appears committed to growing it. With only 11% debt on the balance sheet the 2.1% dividend yield seems well protected. The current price earnings ratio of 15.8 indicates that Analog Devices is fairly valued based on consensus five-year estimated earnings growth of 10%.

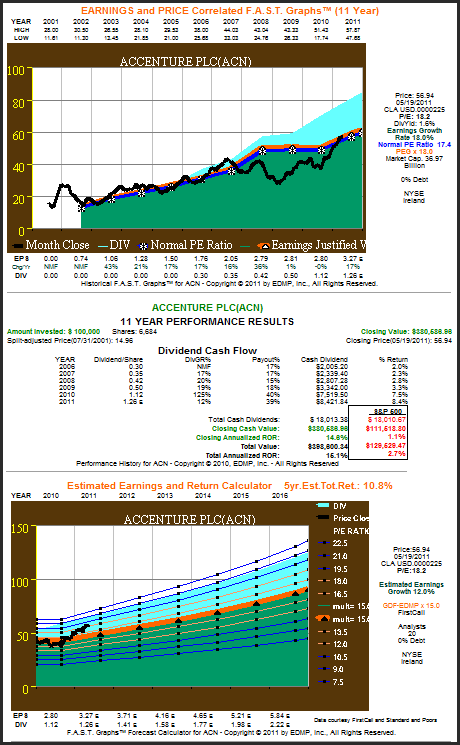

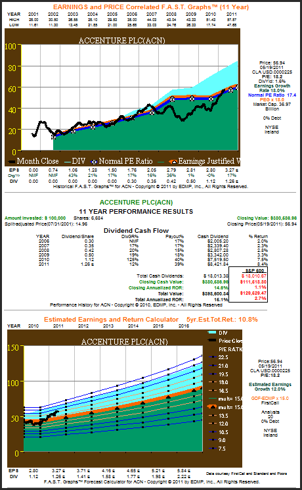

(Click to enlarge)"About Accenture

Accenture is a global management consulting, technology services and outsourcing company, with more than 215,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world's most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$21.6 billion for the fiscal year ended Aug. 31, 2010."

The graph on Accenture (ACN) depicted the most consistent and fastest earnings grower of our group. They instituted their first dividend in calendar year 2006, and it has rapidly grown ever since. The current payout ratio of approximately 40% is consistent with what one would expect from a typical dividend growth stock. The consensus five-year estimated earnings growth rate of 12% is the third-highest of this group; however, their current PE ratio of 18.2 is also the highest indicating that they are fully valued at these levels. The company has no debt on the balance sheet, and operating activity cash flows greater than earnings, indicating that their dividend is well protected.

(Click to enlarge)Summary and Conclusions

With technology so ubiquitously applied to every aspect of our lives today, it's hard to imagine it was only a few decades ago that the industry was born. Consequently, as members of a new industry, information technology stocks have only been considered by investors seeking growth. This made sense, because when starting from scratch this industry, and each of its participants, were hungry for capital to fund their rapid expansion. Therefore, every dime's worth of profit was initially reinvested into the business leaving nothing for dividends. However, as their many factories and infrastructure are now, for the most part in place, many established technology companies are now behaving in the same manner as any traditional business. The once unthinkable act of paying dividends to their shareholders has now become a reasonable allocation of capital.

Technology stocks for growth and income is a relatively new concept. However, it appears to be a concept whose time has come. Although technology stocks cannot boast about many decades of consistently increasing their dividends like many blue-chip stalwarts can, those days may be in front of them. A decade or two from now it's certainly feasible that many well-known information technology companies will become members of the elite lists such as the "Dividend Aristocrats" or the "Dividend Champions," representing companies that have increased their dividend every year for 25 years or more. Time will soon tell whether the information technology sector is up to the task.

As a caveat, it's important to consider the cyclical nature of this industry. Technology changes rapidly, and with those changes the fortunes of any respective information technology company can rapidly change as well. Investors seeking growth of their dividend income should proceed with caution. Historically, the best dividend growth stocks have come from the companies with the most consistent and predictable earnings growth. On the other hand, the information technology sector is capable of providing a faster growth rate than the traditional blue-chip stalwart. Therefore, the total return to include dividends could potentially be quite rewarding. These 10 tech stocks are offered as a potentially attractive group, pending a more comprehensive research effort. The principle caveat emptor (let the buyer beware) applies.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Disclosure: I am long MCHP, ACN, INTC.