In my most recent article titled The 'Magnificent Seven' Dividend Growth Stocks Overlooked by the Stock Market," there were two comments by readers that struck a nerve. To be clear, neither comment disturbed or offended me. Instead, they motivated me to go even deeper into the concept of the importance of valuation than I have in the past.

The first comment was made by David Van Knapp, the number one opinion leader under the category Income Investing Strategies, and therefore, a highly regarded author on Seeking Alpha. In his comment he called me, and I quote, "Mr. Valuation." I took this as a great compliment, because I believe that valuation is one of the most important principles of investing, yet often overlooked and even ignored by many investors.

The second comment was made by a regular reader of my work, and prolific Seeking Alpha commentor who goes by the handle “chowder.” Regarding my article, “chowder” made the following observations and comments:

" I want to comment on a statement you made. My comment is not a criticism of one's investing style. It is simply a philosophy I go by and thought I would share it, for those who may be interested.

You said ... >>> even though I have always admired these great companies, which I now dub the “Magnificent Seven,” I have rarely owned them because the markets have normally overpriced them. <<<

In my opinion, value investing is often confused with buying stocks cheaply."

Then later “chowder” added these additional remarks and clarifications, and it was this part that really inspired me to write this article. Without meaning to, I'm sure, “chowder” through his words, attempted to devaluate what I consider to be the monumentally important, and even perhaps vital, concept of valuation. These are his words:

"If we are to look at the PEP chart for example, in the last 15 years it very rarely saw price below the earnings line. By your own admission, you say the market overpriced your Mag 7.

Maybe we are too strict with our definition of value, especially if one is looking at building an income flow as opposed to total return where one may sell their shares.

If I purchased PEP 15 years ago (I didn't btw), was I getting a good value? I would have had 15 years of increasing dividends that have compounded and to lose 15 years of compounding isn't something I wish to lose because I can't buy cheap.

In my opinion, sometimes you have to pay up for quality. Again, in your own words ... they are great companies."

Now, before I go any farther, let me just say again that “chowder” is a regular reader of, and commentor on my work, and that I have a great deal of respect for his opinion and ideas. Therefore, his comments in no way offended me; instead, they inspired me to more vigorously champion my "cause" - The importance of valuation. However, I disagree with his concept of being willing to, or needing to "pay up for quality."

The remainder of this article is designed to illustrate that you can pay too much for even the best of companies, and more importantly, you don't have to. Our contention is that in every market, whether bull or bear, there will be overpriced, fairly priced and underpriced companies. Therefore, it's the job of the investor to search out the fairly priced or underpriced companies, and avoid the overpriced.

The impact of getting valuation right

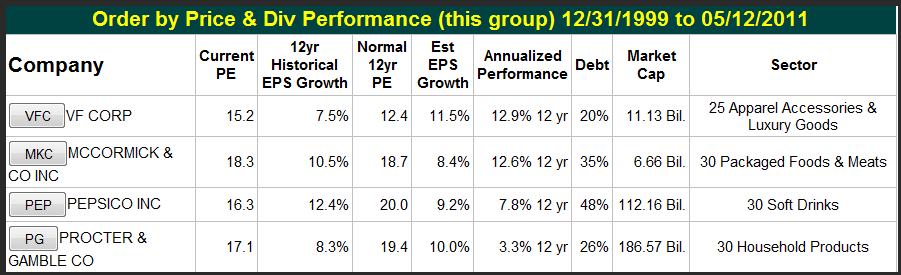

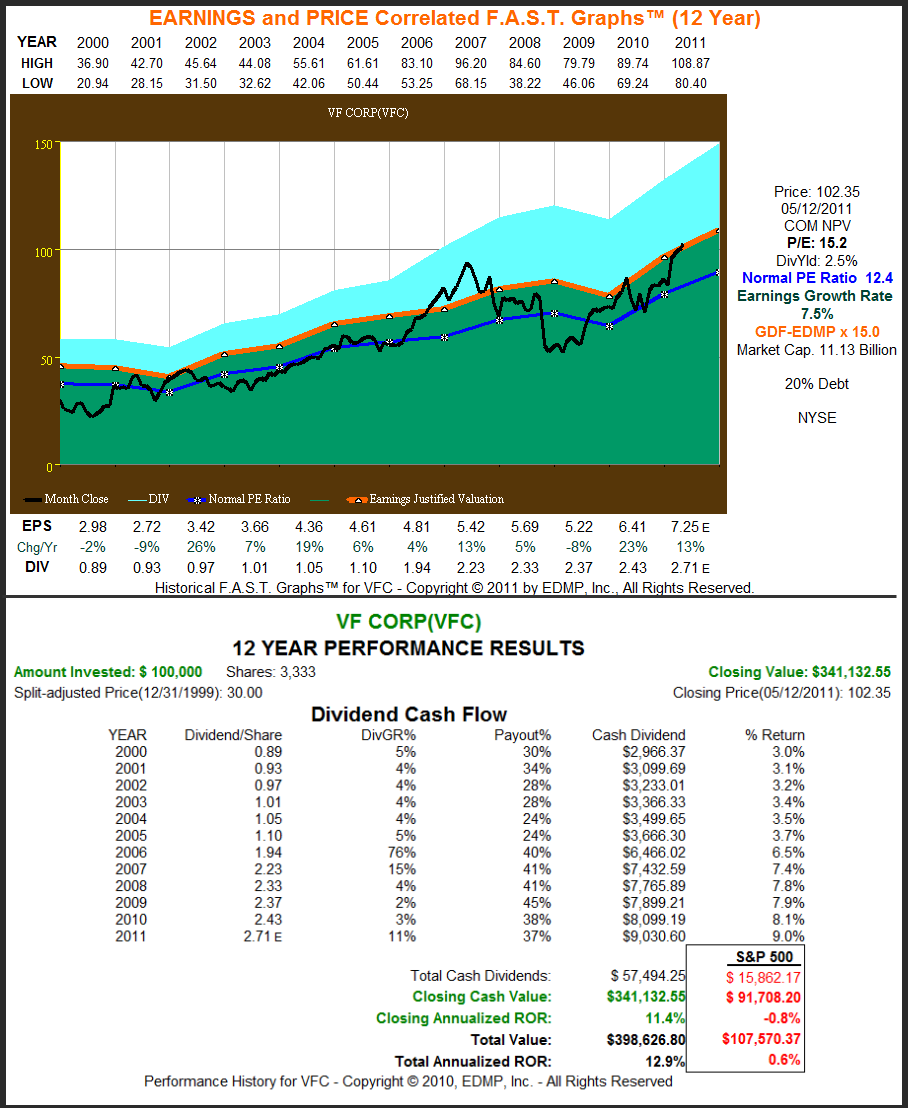

The following table, produced by our F.A.S.T. Graphs™ research tool, lists four blue-chip dividend paying companies in order of highest to lowest total return since calendar year 2000. There are several interesting facts that support the importance of valuation that can be gleaned from the table. First of all, these companies are also listed in order of lowest starting valuation to highest, thereby illustrating that the lowest starting valuation produced the best results.

Also, notice that the highest annualized performance was generated by VF Corporation (VFC), the company with the lowest historical EPS (earnings-per-share) growth rate. But perhaps most importantly, notice how Procter & Gamble (PG), the most overvalued of the group, generated a very anemic total return. Finally, the reader should also notice that each of these companies are industry-leading blue chips and members in good standing of David Fish’s list of dividend champions (companies that have paid dividends for at least 25 straight years).

(Click charts to expand)

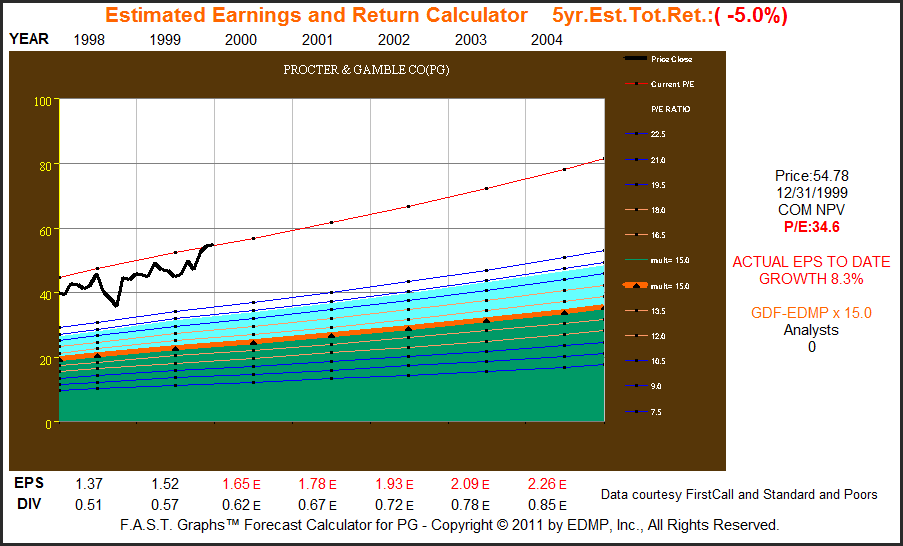

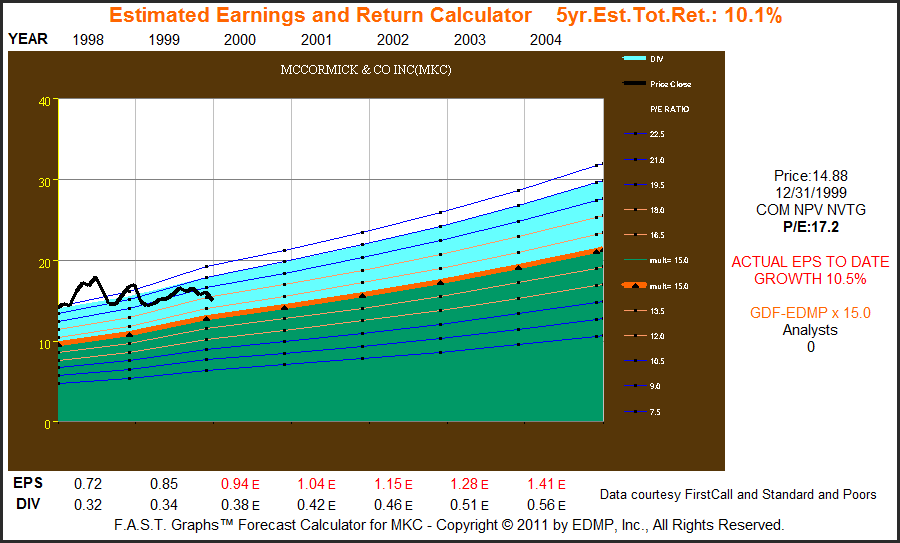

One of the great advantages of our graph research tool is the ability to look back in time and be able to examine what valuations of various companies may have looked liked. The following four graphs look at our four example companies at calendar year-end 1999 through the lens of our estimated earnings and return calculator. However, when the “estimated earnings and return calculator” is used historically, it morphs from an estimator tool into a measurement of actual historical results.

Therefore, notice that to the right of each example company’s graph the actual EPS growth rate through yesterday's date (May 12th, 2011) is calculated and provided. But most importantly, note that each example’s price earnings ratio on December 31, 1999, is also listed. Consequently, from the table above you can compare each company's historical normal PE ratio with its PE ratio on December 31, 1999.

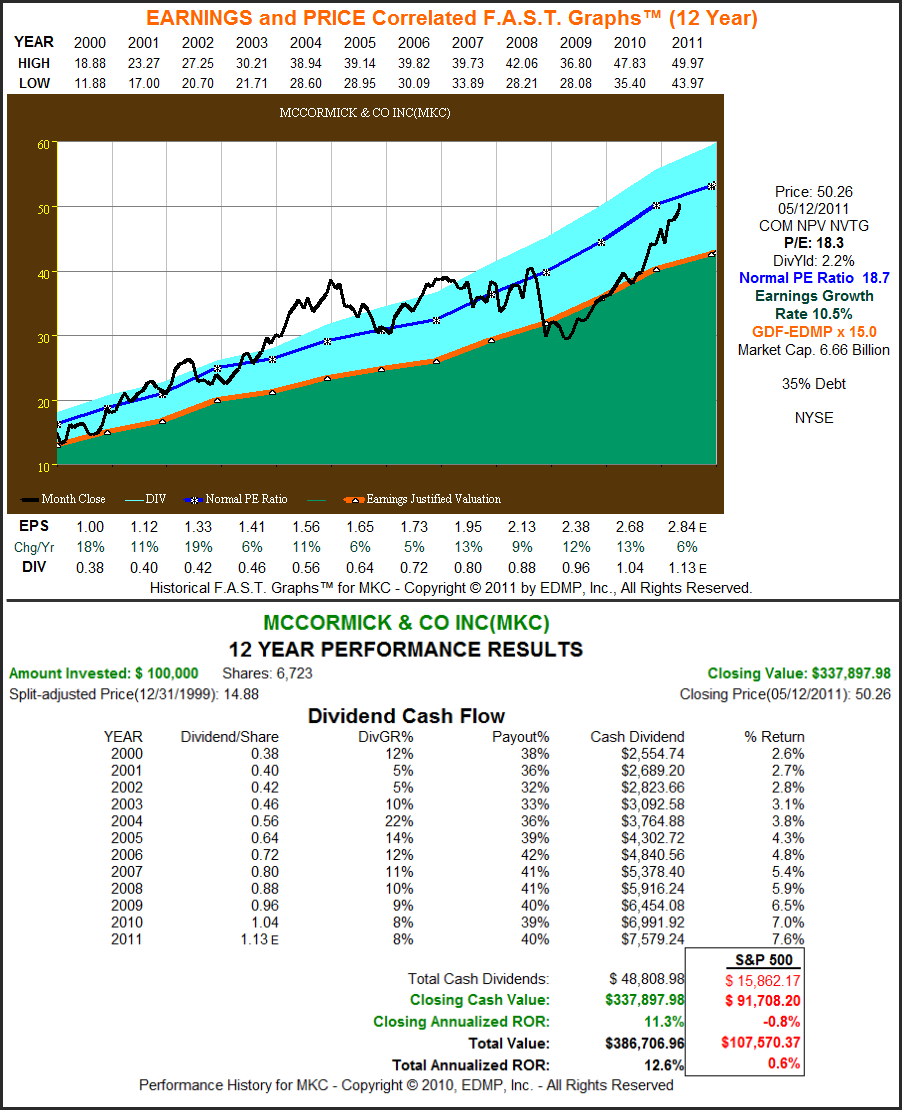

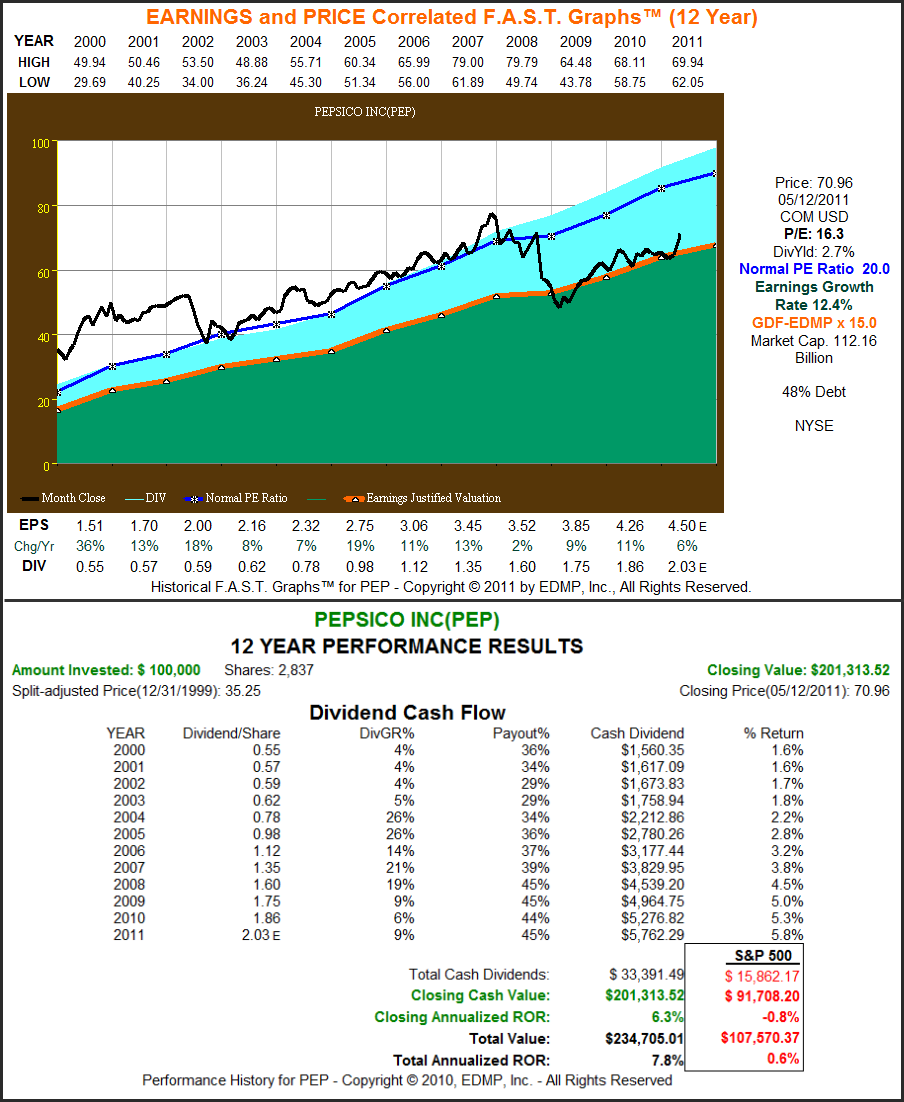

From this we can see that two of our examples were overvalued on December 31, 1999; Procter & Gamble (PG) and PepsiCo (PEP). Procter & Gamble's normal historical PE ratio is 19.4, but on December 31, 1999, it was 34.6. PepsiCo's historical normal PE ratio was 20, but on December 31, 1999, it was 31.8. One of our examples, McCormick & Co. (MKC) was fairly valued. McCormick's historical normal PE ratio was 18.7, but on December 31, 1999, it was 17.2, indicating fair value to slight undervaluation. And our last example, VF Corporation (VFC) was very undervalued, its historical normal PE ratio was 12.4, but on December 31, 1999 it was only 9.9.

The point we are attempting to make here, is that overvaluation, fair valuation and undervaluation would have been evident and determinable for each example listed. So even though year-end 1999 was the beginning of the end of the irrational exuberant period, when most stocks were overvalued, both fair value and undervaluation was to be found. Thereby providing evidence of the intelligence of building a portfolio one company at a time, in contrast to having a bias on the overall market.

Valuation is a mathematical principle and not a vague concept

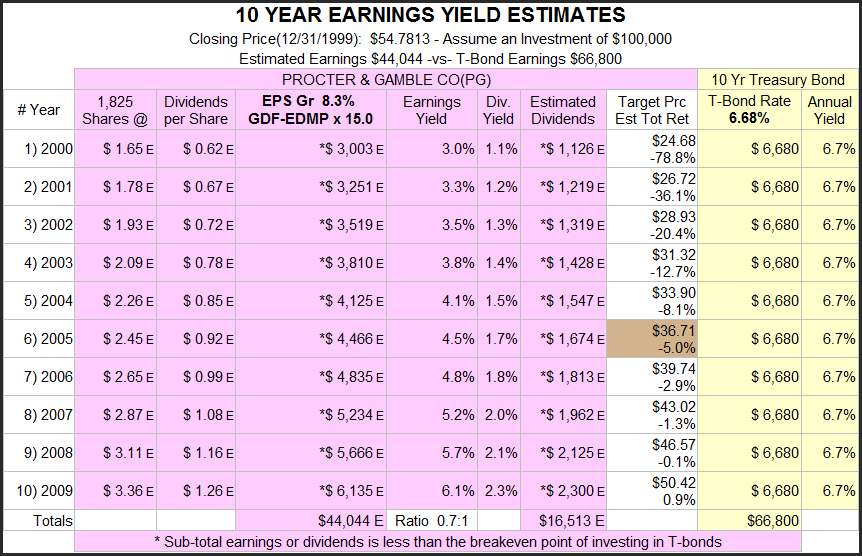

When I speak of valuation, I am referring to the mathematical calculation of the returns, which include both capital appreciation and dividend income, which you could prudently expect to earn from the company's cash flows (earnings). Those returns should be large enough to compensate you more than you could earn from a theoretically riskless investment like a Treasury bond. If you are not being compensated for the extra risk you're taking by investing in stocks, then we believe you are paying more than you should be.

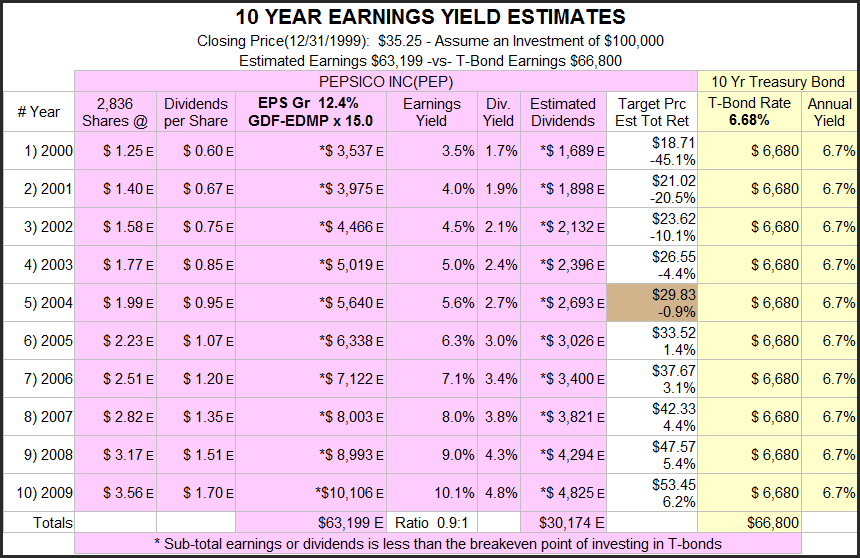

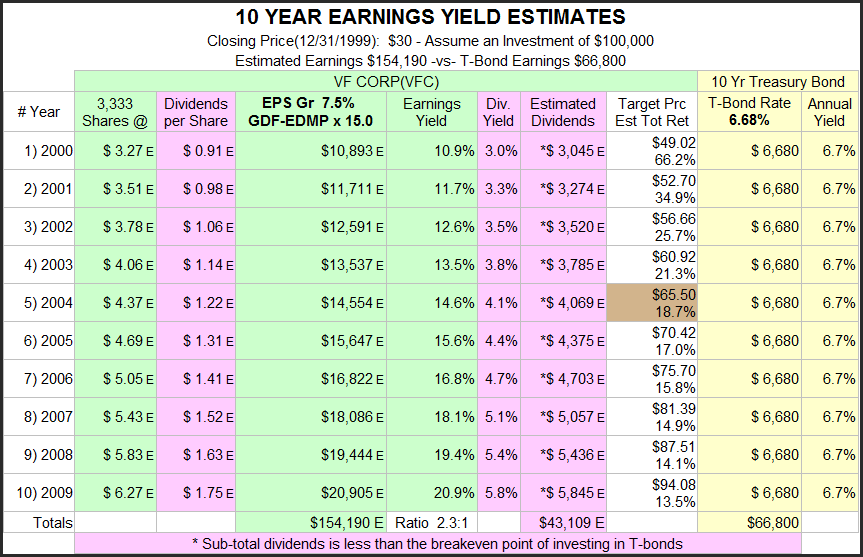

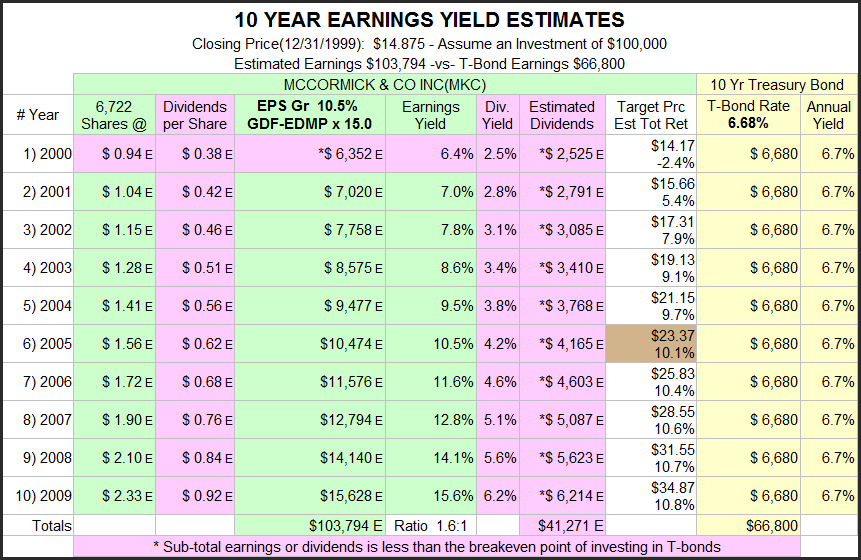

The following four earnings yield estimates graphs are associated with the four estimated earnings and return calculator graphs presented above. Instead of being a forecast graph, they also represent and depict actual results since calendar year-end 1999 when reviewing historical periods.

There are two columns we would like to focus the reader's attention on with these graphs. The first is the column marked earnings yield, and the second is the 10 year Treasury Bond annual yield, or the last column. What these columns illustrate is the actual earnings yield that each of our four example companies offered investors at the time.

When the earnings yield column is pink, like it is with Procter & Gamble and PepsiCo, this means that overvaluation is evident. In other words, the total cumulative earnings of these two companies was less than the riskless interest you could earn on a 10 year Treasury Bond. Also, keep in mind that not all of the company's earnings are paid out (see the final four graphics below) whereas the Treasury Bonds interest is. In contrast, both VF Corp. and McCormick & Co. offered earnings yields that compensated the stock investor for the risk they took.

Sound valuation lowers risk, increases dividends and total returns

The final four complete graphs below illuminate both the importance and the benefits of sound valuation as an important investing principle. This final set of graphs is listed in order of best or lowest valuation to worst or highest valuation since year-end 1999. There are several important takeaways that can be gleaned from studying these graphs. Notice that the first year's dividend yield (calendar year 2000) was the highest for the two companies with the best overall valuation. As a result, the two companies with the best overall valuation also generated the highest level of total cash dividends paid over the 12 year period.

Another very interesting investing principle that can be gleaned from this analysis is how VF Corporation, with the lowest historical earnings growth rate, but best (lowest) starting valuation produced the most dividend income and the highest total return. But most importantly, notice how Procter & Gamble with the worst, or highest starting valuation produced the lowest level of total dividends and the lowest total rate of return. Even though Procter & Gamble's earnings growth rate was slightly higher than VF Corporation, due to excessive overvaluation their total dividend income was less than half that of VF Corporation's and their total return only a fourth of what VF Corporation rewarded their shareholders with.

Conclusion

Valuation matters a lot.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Wikio

No comments:

Post a Comment