The selection of the five banking firms below is based on the following supportive data as well as both their short and longer-term price and earnings performance. I expect these companies to have improved earnings, but I do not have the confidence, price-wise to take new bullish positions.

For guidance, I normally compare most all securities with Apple (AAPL). When the securities get close (in my three disciplines) I buy them confidently. Those disciplines are my weighted fundamental, technical and consensus analysis. I also have just two categories of investments.These are a mix of “Bellwether” and “High Profile" companies and are rated and compared below with brief comments.

The market is doing what it loves to do

Lately, that means it is both fundamentally and technically very fickle. What many investors often forget is that what appears to be a fact is, in reality, very creative fiction. The fictional stories being told by Wall Street and the media are so compelling that the average investor takes the hook, line and sinker most every time. That’s a fact and, for me, it is a very sad commentary.

As mentioned above, earning estimates, on balance, are positive for the near-term, and should be improving noticeably throughout the coming year. However, you might remember that the way the "Street" will reward or punish any company in the future is always questionable.

My analytics, to a large degree, has to do with a wide range of comparative and on-going studies. Comparing these five companies along with their peers and other top/strong growth/revenue producing companies does not provide me with sufficient positives to hold long positions.

The Major Bank industry group, both U.S. and international is quite low on my consensus rankings of over 200 industry groups and is ranked as "currently unfavorable." Therefore, I expect the majority to not hold up well during the coming months.

In the tables below you will perhaps see why my valuation approach offers data that I believe can produce profitable investments for the intermediate and longer-term, however definitely not over the near-term. Integrating information and data that is "technical and consensus analysis" is also very important to near-term investment decisions.

Valuation Analytics Table

Major Bank - General Industry Group:

Stock and Symbol | Approx. Current Price | My Target Price % Above (+) / Below (-) Current Price – Valuation is "Tweaked.” One Year Projections are from the next - - Bullish Inflection Point. | PEG | P/E | Forward P/E | Valuation Divergence (%) One - Year Projected from a Mean – Sigma and from the next - - Bullish Inflection Point. |

1. Bank of Am.(BAC) | 14.8 | 30% to 50+% | 1.37 | 17.7 | 7.9 | 100+% |

Comments: This is an "excellent" valuation and not a bad long-term target price projection. However, adding the technical and consensus analysis, you have a confirmation that BAC is currently just another banking company in trouble! | ||||||

2.Citigroup,(C) | 4.9 | 20% to 40% | 1.85 | 14.1 | 9.1 | 54% |

Comments: This is an "excellent" valuation and not a bad long-term target price projection. However, adding the technical and consensus analysis, you have a confirmation that C is currently just another banking company in trouble! | ||||||

3.KeyCorp,(KEY) | 9.7 | 25% to 45% | 3.03 | 21.7 | 12.7 | 71% |

Comments: This is an "excellent" valuation and not a bad long-term target price projection. However, adding the technical and consensus analysis, you have a confirmation that KEY currently is just another banking company in trouble! | ||||||

4. PNC Financial,(PNC) | 64.6 | 10% to 20% | 1.80 | 10.6 | 10.2 | 6% |

Comments: This is a "poor" valuation and target price projection. However, when you do further Fundamental studies it looks much better. Add to that, the technical and consensus analysis and you have a confirmation that PNC may well remain a winner! | ||||||

5. State Street,(STT) | 45.7 | 10% to 15% | 1.27 | 13.4 | 10.7 | 25% |

Comments: This is a "good" valuation and not a bad long-term target price projection. However, adding the technical and consensus analysis, you have a confirmation that STT is currently just another banking company in trouble! | ||||||

Summary of the Three Disciplines:

Company Symbol | Category | Fundamental (weighting 40%) | Technical (weighting 35%) | Consensus (weighting 25%) |

1. BAC | Bellwether | Excellent | Good | Good |

2. C | Bellwether | Very Good | Good | Good |

3. KEY | High Profile | Very Good | Good | Good |

4. PNC | High Profile | Poor | Very Good | Very Good |

5. STT | High Profile | Good | Good | Poor |

The general market is currently over-valued, over-bought and is showing signs of deterioration, especially in the area of breadth. Interest rates are on the rise and inflation is already a serious problem. This means that you must consider holding cash or perhaps taking bearish positions. I would not recommend taking bearish positions in any of these securities quite yet.

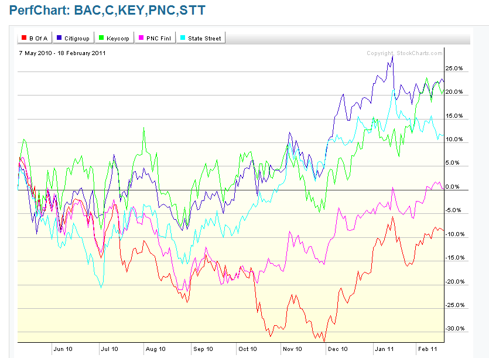

For a current (up to the minute) chart of BAC and C, click here and scroll down.

My focus is "investing wisely," e.g. taking advantage of the bull/bear cycles as they occur within the overall marketplace. Integrating modern fundamental analytics within these technical cycles means maintaining a process of the thorough and ongoing analysis of many companies and industry groups. I believe this is a vital discipline in "investing wisely.”

Source information and data:

- Yahoo Finance

- MSN Money

- MorningStar

- BarCharts

- StockCharts

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Only Mr. Bauer can look at the banking and financial sector and compare it to a technology stock. The fact that he arrives at conclusions based on these comparisons is troublesome.

Why not compare the five banks with Wells Fargo? Mr. Buffet has recently increased his stake in WFC, it would make a timely article.

I have asked repeatedly how Mr. Bauer compares the incomparable. Instead of a detailed explanation of how and why all of his stock selections are compared to aapl, he continues to publish articles using this method.

Mr. Bauer, please explain how your comparisons are valid. Please inform me of how a bank stock or pharmaceutical stock can be measured by Apple.

Thank you.

If the economy continues on the present rate we might make it with the projections about 10 years from now but if we take another dip all bets are off for B of A.

I am long C; my view is this investment is a longer-term speculative play. My tendency is to review the fundamentals, and use technical analysis as a confirmation or counter-point.

Citi appear to have reasonable risk-reward given consensus earnings estimates and applying a market-mean PE multiple. This is coupled with recent remarks that the bank plans to return capital to investors in 2012. Vic Pandit is focusing the company on the international stage, shrinking the base, and better managing risk.

The two-year weekly chart looks good, too. MAs, MACD, OBV all looking positive.

So why is the data weak enough to state, "...Comparing these five companies along with their peers and other top/strong growth/revenue producing companies does not provide me with sufficient positives to hold long positions."

The banks seem to be in at least neutral shape based upon the economic cycle and no inclination (yet) of the Fed to tighten monetary policy. Citi has some unique factors that may trump even modest tightening. No?

While Apple is a market leader or "general," I likewise to some other readers find it difficult to compare AAPL with banking securities. I generally try to compare equities within the same sector.

To the author: you're just a blogger.

The editor knows nothing about finance or anything else. The editor just checks on grammar and spelling.

1) Comparing different industries with different models and metrics is amateurish.

2) Technical alalysis has been proven to be faulty for several decades. Imagine comparing two companies with similar charts and ignoring the fact that their businesses and balance sheets may be radically different -- tea leaf anf taro card set.

3) Consensus is rarely correct. The number of companies that beat or disappoint earnings each quarter is significant.

Long C and BAC

I love AAPL, but it will not double in the next year unlike some of the financials. The banks are about to break out.

1. Nationally, Realtor reports of sales are significantly inflated, inventory of residences on the market is significantly understated, and inflation/interest rates are currently rising. Expect a double-dip in the national Residential Real Estate Market, and more loan losses.

2. The unrest in the Middle East will raise oil prices, as will the decline in the US Dollar. WHEN oil reaches $100+, growth will slow and disappear. Reducing lending

3. China has a Real Estate bubble of it's own, and their Command Economy will need to make changes to adapt, once the bubble breaks. Increasing volatility.

4. The US Congress does not seem to understand that it Really, Really needs to balance the budget, and bring back the US capital stuck overseas. We are already half way through the Federal fiscal year, without a budget. This is not re-assuring, and makes it difficult for companies to plan.

Bottom line: When the tide goes out, all boats drop. I'm sticking with short term trading on the banks: Buying on the dips and selling if I have gains of more than 1% in a day, 2% in a week or 4% in a month. I'm also sticking with NLY,CIM and AGNC, keeping them for the dividends, unless the capital gains from buying on the dips exceed the dividend to be earned.

Sold 30,000 shares C last week at 4.92+. Looking to buy at 4.80-. Holding period: about 1 week. Annualized return: about 150%

BAC continues to write-off all they can to get the financial crisis behind them. These losses are goodwill impairments, reserves and mandatory set asides for litigation that is turning positive for them in many cases. But, the cash flow continues.

When they are given the green flag - I look for a modest increase in the dividend - then some better more realistic valuation according to their LT prospects should take hold.