Halfway through the first quarter of 2011, we are exceeding my expectations, though I am probably not alone on that front. I shared my very bullish views for the year initially in early October, suggesting that we could see 1500 on the S&P 500 in 2011. I followed up recently with a different way of arriving at the same conclusion, suggesting thatdividend growth would fuel market gains. While it's premature to declare victory, I remain very confident that we will continue in this direction. As of Monday night, the S&P 500 is up almost 6%. At this pace, we will exceed the approximate gain of 20% that I am forecasting, though we will most likely see some consolidation later this quarter and certainly throughout the year.

Looking at the dynamics of the overall market, large-caps are doing quite well. The very largest stocks aren't leading the way, but they sure are doing a nice job of keeping up. We can see this by looking at the Russell data, which shows that the R1000 is up 6.36% on a total return basis (not too far from the S&P 500's 6.18%). The R2000 is up 5.48%. It turns out that the mid-caps are faring the best, with the Russell Mid-Cap, which represents the 800 smallest names in the R1000, up a stunning 6.93%. Still the other 200 aren't doing badly at all, with the Top 200 index up 6.16%. To me, market cap isn't really a factor at this point. One factor that does jump out is that Growth is beating Value across all market caps. It seems clear that investors are finally willing to make a bet that the economic expansion has legs.

Today I want to explore yet another argument that supports my bullish view. While I spend most of my time trying to uncover individual stocks that offer potential market-beating returns (usually small and off the beaten path), I confessed near the end of the year that large-caps stand out for being cheap. While I don't expect that they will necessarily beat small-caps, it should be a pretty good race over the balance of the year. In fact, I have moved my Top 20 Model Portfolio to the highest large-cap exposure that I can recall, with 5 names currently above $10 billion and 3 greater than $100 billion.

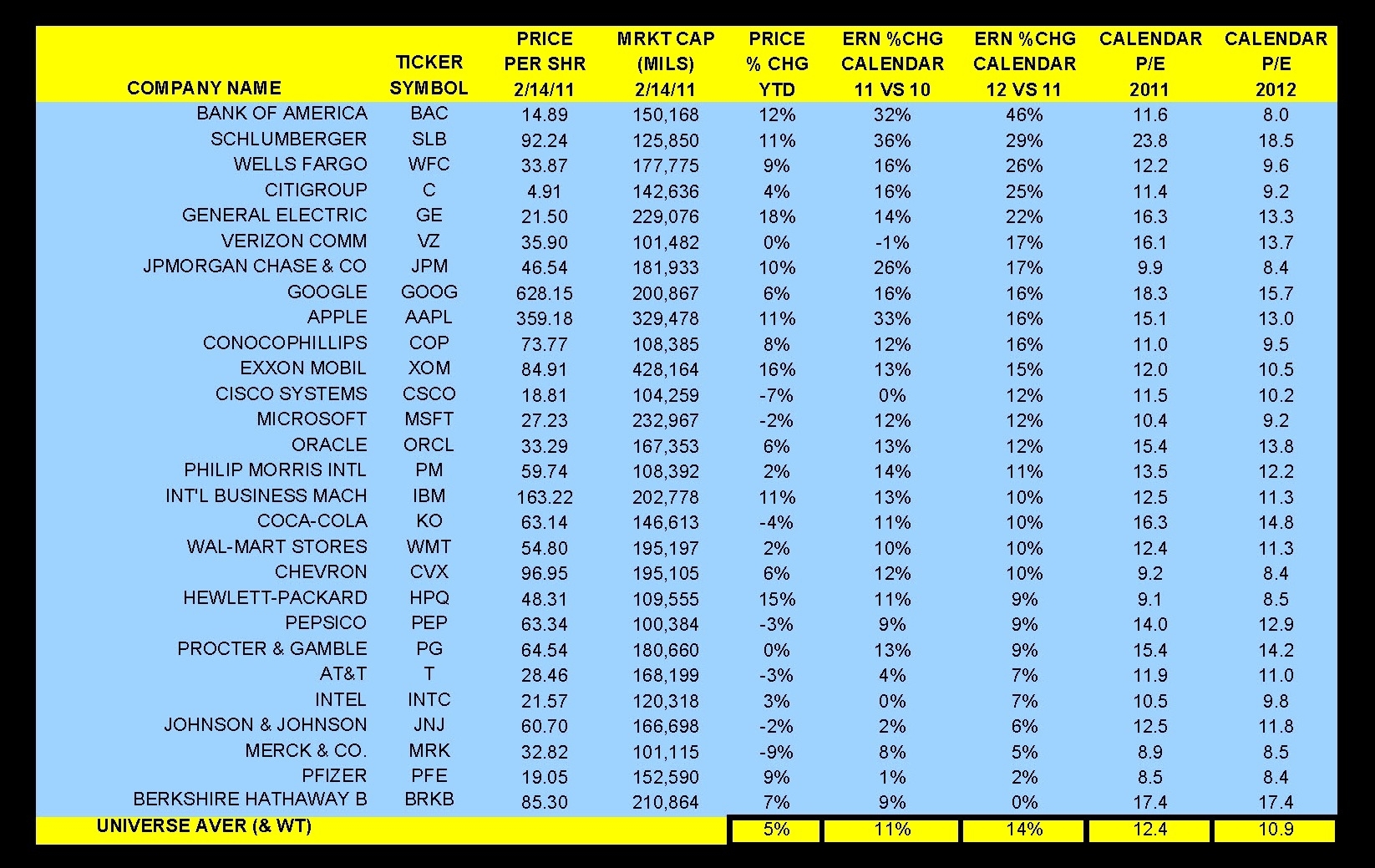

I think if we take a look at the very largest companies in the S&P 500, it becomes very clear that my 1500 target might prove conservative. There are 28 names that have market caps in excess of $100 billion - mega-caps. In total, they represent over $4.8 trillion in value or 40% of the value of the S&P 500. So, it seems like getting a good feel for these 28 names might give us a good handle on the overall market.

The 28 mega-caps in the S&P 500 are cheap. On a PE basis, they trade on average as well as on a market-weighted average at about 12.5X 2011 estimated EPS. The average stock has a dividend yield of 2.2%, substantially higher than the overall yield on the S&P 500 of 1.8%. What's most interesting, though, is that analysts are expecting double-digit growth this year to be followed by slightly higher double-digit growth next year, as you can see in the table below:

I have ranked the names on 2012 projected earnings growth. There are 11 names currently forecast to grow earnings in excess of 15%, with a very healthy average of 14% and median of 12%. Yet, the 2012 PE for the group is a paltry 11X. Only one stock trades at a 2011 PE in excess of 20, and it's growing like gangbusters. We can argue about what the exact earnings growth in 2012 might be, perhaps slightly less than expected, but what seems clear to me is that there is plenty of room for multiples to expand. I didn't include it in the table, but sales growth is supposed to be 6%, suggesting a combination of margin improvement and share repurchases most likely accounting for the higher earnings growth. This makes sense given where we are in the economic cycle (margins should expand) and in the capital cycle (these companies can add leverage - the net debt to capital for the group is a median of just 17%).

I think that we can get a sense of the tremendous upside to the market by focusing just on these largest of the large-caps. With a decent 10-year corporate bond yielding less than 4.5%, the 8% earnings yield for the mega-caps (the inverse of the 12.4PE) jumps out as excessive. The valuation of these stocks appears to price in substantially higher interest rates or earnings declines, while the most likley scenario is modestly higher rates and earnings growth.

As I look at these names, several would seemingly offer up to 50% or higher returns over the next year, while most would seemingly offer at least 20% upside. As I mentioned earlier, I am including several of these in my model portfolios at InvestByModel, including Chevron (CVX), with a 141 target, Cisco (CSCO, with a 28 target, Intel (INTC), with a 31.50 target, and Johnson & Johnson (JNJ), with a 83 target over the next year.

If we do the very simple exercise of projecting that the 2012 PE rises to the current PE, we should see prices rise about 15% from here, which is consistent with my overall forecast of 1500 on the S&P 500 (we are currently at 1329). It seems, though, that this may be too conservative. If you agree with my argument but prefer an ETF to take advantage of the cheapness in mega-caps, I would suggest Rydex Russell Top 50 (XLG) - don't you love that symbol?

Disclosure: I am long CSCO, CVX, INTC and JNJ in one or more models at InvestByModel

No comments:

Post a Comment