Dividend Growth investing is one of the most misunderstood investment strategies out there. Yet various studies have proven that quality dividend growth stocks tend to outperform the broad market indices over time.

The main obstacle to understanding dividend investing in general is that dividend stocks are equities and not a separate asset class. Companies exist for the benefit of shareholders, which means that they have to generate some return either in the form of dividends or in the form ofcapital gains. Paying a dividend instills discipline on management to be careful with the cash position and not take excessive risks such as ill-timed acquisitions or investing in projects which might not generate sufficient returns for the company. Investing should be all about the middle ground, and not excessive assumptions about relying exclusively on capital gains or exclusively on dividends. Everything is good in moderation, and investing should not be any different.

Dividend investors realize that focusing just on the dividend income is not preferred. In order to be able to pay the dividend, a company needs to have a sustainable income stream, which preferably could grow over time. This would support a growing dividend over time. A growing stream of earnings also means that unless an unjustifiably high price was paid for the stock, its price should rise over time as well. By reinvesting dividendsinto purchasing more shares, and by enjoying capital gains in the process, investors will be able to take full advantage of the power of compounding, which will help them in achieving higher net worths over time. The point that dividend stocks are equities and that compounding a smaller initial investment at a certain return could lead to a higher invested amount over time is missed not only by ordinary investors, but even some financial writers.

Another misunderstood fact is that a company that grows distributions over time, could generate sufficient yield on cost to its early investors. If one invests $500,000 today in dividend stocks which yield 3%, they would be generating $15,000 in dividend income. If dividends grow at 6% per year for 12 years, the dividend income would be $30,000 in 2023. This income stream would be the same as the income stream generated by a $1,000,000 investment in 2023, yielding 3%. Dividend growth is not a given of course, although it has been a fact of life for the past several decades, and that is for broader market indices.

Dividend stocks do have risks of course. There are no risk-free assets to invest in to begin with however. Even investing in US Treasuries, which are viewed as fairly low risk, could lead to losses if interest rates increase, the dollar loses purchasing power or the US government fails to meet its obligations. Investors could lower their risks by diversifying into at least 30 individual stocks representative of as many market sectors as applicable. A long record of consistent dividend growth is a must, coupled with a business model that boasts strong competitive advantages, stable and growing earnings and strong brand recognition. Overpaying for stocks is a sure way to increase risks of investment losses, just like chasing the highest yielding stocks without checking whether the payout is sustainable is a recipe for disaster.

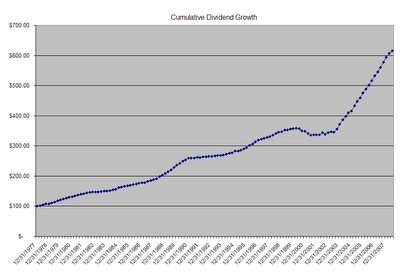

Even when one looks at the dividends per share in the S&P 500 over the past 30 years, a clear trend of dividend growth is obvious. Dividend growth investors are simply playing on that trend by investing in the companies that actually do grow dividends over time. Not all companies that are purchased by investors would keep growing distributions over time, but if a careful selection method is utilized by investors, coupled with a sound diversification policy, a dividend portfolio should be able to generate high income over time.

click to enlarge

As mentioned above, dividend growth is a function of earnings growth. Companies make more money by expanding, raising prices at a higher pace than the increase in costs, cutting costs, acquiring companies or by a combination of any of the above. A gradual decrease in the dollars purchasing power due to inflation actually benefits equities, since this makes nominal prices higher, even if the product or service was acquired at lower nominal amounts. In addition to that, as the number of consumers in the world increases, this could only benefit global companies such as Procter & Gamble (PG), McDonald’s (MCD), Johnson & Johnson (JNJ), Coca Cola (KO) or Colgate-Palmolive (CL).

McDonald's Corporation (MCD), together with its subsidiaries, operates as a worldwide foodservice retailer. It franchises and operates McDonald's restaurants that offer various food items, soft drinks, coffee, and other beverages. The company has raised distributions for 34 years in a row and has a ten year dividend growth rate of 26.50% per year .Yield: 3.20% (analysis)

Johnson & Johnson (JNJ) engages in the research and development, manufacture, and sale of various products in the health care field worldwide. The company operates in three segments: Consumer, Pharmaceutical, and Medical Devices and Diagnostics. The company has raised dividends for 48 years in a row and has a ten year dividend growth rate of 13% per annum .Yield: 3.60% (analysis)

The Procter & Gamble Company (PG) provides consumer packaged goods in the United States and internationally. The company operates in three global business units (GBUs): Beauty and Grooming, Health and Well-Being, and Household Care. The company has raised distributions for 54 years in a row and has a ten year dividend growth rate of 10.90% annually. Yield: 3.00% (analysis)

The Coca-Cola Company (KO) manufactures, distributes, and markets nonalcoholic beverage concentrates and syrups worldwide. It principally offers sparkling and still beverages. The company has raised dividends for 49 years in a row and has a ten year dividend growth rate of 10% per year. Yield: 2.70% (analysis)

Colgate-Palmolive Company (CL), together with its subsidiaries, manufactures and markets consumer products worldwide. The company has raised distributions for 47 years in a row and has a ten year dividend growth rate of 12.40% per year. Yield: 2.70% (analysis)

Full Disclosure: Long MCD, CL, KO, PG, JNJ

Recommends

More on Investing for Income »

Thanks for presenting a compelling case for dividend growth investing, along wit some of the best Blue chip examples, which have proven the strategy's soundness over many years.

INTC offers 3.3%

Great growth , great profit, and the Price of the stock is a nice move north.

I try to use the charts to help make decisions.

When an article is unfavorable to dividend investing, this community unites to defend dividend investing...nothing wrong with that; however the community also seems to give a pass to favorable articles that also include a faulty premise...here's one from the article above:

DGI establishes the theme of his article in the lead to the 2nd paragraph..."The main obstacle to understanding dividend investing in general is that dividend stocks are equities and not a separate asset class."...really?

So investors mistakenly think dividend stocks are actually bonds?...or derivatives?...maybe commodities?...and if investors knew that dividend stocks are actually real stocks, they would rush to buy more of them because they are more compelling than are any of the alternatives that do not pay a dividend, right?

I ask what, exactly, is the basis for assuming that investors don't know that dividend stocks are equities?

(p.s. an anecdote about your aunt Sally is not evidence)

I would almost go the other direction that dividend companies are NOT classified as an equity for purposes of how they are used and evaluated in a portfolio. They share characteristics of both bonds and equities.

"Overpaying for stocks is a sure way to increase risks of investment losses, ..."

drives me a little crazy. While I don't necessarily disagree with the statement and I've seen lots of comments defending "not paying too much", how is that value determined... exactly? What is the golden formula that tells you that you might be paying too much?

Forward or trailing P/E ratio? Price/sales? Price/book? Price/cash flow, etc?

My problem is that determining that "overpaying for stocks" is subjective as there is no exact formula to determine this. Everybody seems to come up with their own determination. Maybe I'm missing something so if there is a definitive formula, I'd love to see it.

Claiming that a P/E of 50 is too expensive might be accurate but how does one know exactly?