Going for Growth (Part 3): Forecasting Future Earnings the Key - Seeking Alpha

Introduction

It is my belief that as investors in common stocks, and whether we are aware of it or not, we are all buying earnings. Because ultimately, long-term investor rewards are going to be a function of two primary factors; the most important of which is the earnings power of the companies invested in. The stronger and faster that a business can grow their profits, the more valuable it becomes to the shareholders. Furthermore, if income is the goal, the level and rate of growth of dividends are also directly tied to earnings growth. The second important factor is valuation. If you find a company with good earnings power, you should do very well over the longer-term, as long as you don't do something foolish like over pay to buy those earnings. This is why I emphatically state, you make your money on the buy side.

When the above principle is applied to my definition of a growth stock, the following dynamic is revealed. If you buy one dollars worth of earnings today, with the expectation of 15% earnings growth, then your future earnings five years out would be two dollars. In other words, at a 15% growth rate it takes approximately 5 years to double your earnings. If you expect 20% growth, then your dollars worth of earnings you bought today will grow to two dollars worth of earnings in just over 3 1/2 years. And if you're lucky or smart enough to find a company capable of growing earnings at 25% per annum, then you will have two dollars worth of earnings in just under three years. The exceptional future returns that can be derived from either of the examples above, is functionally related to the significantly greater earnings power you then possess and achieved over such a short period of time. These examples represent quintessential validation of the phrase - time is money.

A few comments on analyst estimates

In Part 2, I provided several examples of future earnings expectations based on consensus analyst estimates. I have found there to be a lot of confusion and misunderstanding regarding the accuracy and validity of analyst estimates. I believe the problem rests with the manner in which misses and beats are scored. In truth, I feel it is unreasonable to expect future earnings estimates to be too precise. All one should really ask is that the estimates provide a reasonable range of achievable and acceptable probabilities and accuracy. In other words, if the consensus estimate says the company will earn $2.00 per share, and the company reports $1.98 per share, this is generally considered a miss. In my view, the example above was an accurate estimate within a reasonable plus or minus range.

Therefore, I would like to see a study where analyst estimates are scored based on achieving an accuracy rate of plus or minus 5%, then plus or minus 10%, then plus or minus 15% and so on. I believe a study like this would show a significantly higher percentage of accuracy of analyst estimates than most studies currently suggest. However, the real point I'm trying to make is, that although I believe analyst estimates are more accurate than most people give them credit for; I also believe that they only represent a good starting point prior to a more comprehensive research effort. In other words, the analyst estimates offer a great screening function, but before I will lay my money down, I need to validate their expectations in my own mind.

Forecasting Future Earnings is the Key

As investors, I believe we cannot escape the obligation to forecast; our future results depend on it. However, our forecasts should not be mere prophecy or simple guessing. We should not play hunches, instead, we should attempt to calculate reasonable probabilities based on all the factual information that we can assemble. Even then we should acknowledge and understand that the best we can do is develop forecasts that will fall within a reasonable range of probabilities. My objective is to use analytical methods that provide me reasons to believe that the relationships that have produced earnings growth in the past will persist in the future to a level high enough to satisfy my definition of a growth stock. As Warren Buffett so eloquently once put it, "It is better to be approximately right than precisely wrong."

Most importantly, forecasting is a process and the actual act itself can vary significantly from company to company and industry to industry. Therefore, I can only provide concepts and generalizations of the forecasting process that I personally use. Complete books can, and perhaps should, be written on this important subject and vital component of what I consider true investing to be all about. With that said, there are no shortcuts. Whether you are buying growth stocks or dividend paying stocks, or any other investment, you need to have some rational and, hopefully, reasonable expectation of the future. That can only be accomplished, and must be accomplished, by a forecasting process. Therefore, what follows is offered as a general overview and a few simplistic examples of how forecasting future earnings can be approached and accomplished.

I typically approach the forecasting process from both a macro and micro evaluation. With a macro perspective I focus on what I believe are obvious areas that offer major future investment opportunities. For example, a study and analysis of demographics can be quite useful. In the United States, and throughout much of the rest of the world, there currently exists a bi-modal distribution of our population. Here at home this is often referred to as the "Graying of America" and the "baby boomer" generation. A study of the consumption tendencies of these and other demographic segments can allow you to make informed decisions as to the future health of several industries that will serve these large and growing markets. Healthcare and financial services focused on providing retirement benefits are two obvious examples that come to mind. You may have noticed that several of our examples in Part 2 were healthcare related.

Although there are numerous opportunities in healthcare, forecasting the future potential of a pharmaceutical or biotech company is a straightforward but often precarious process. The logical place to start is by evaluating the company's current portfolio of drug candidates in their pipeline, and where they are in the various stages of regulatory filing. Personally, when I do this, I place most of my emphasis on drug candidates in phase 3, and less emphasis on drug candidates in phase 1 or 2. The majority of phase 1 candidates actually fail. In contrast, the majority of drug candidates in phase 3 usually make it to the marketplace. Therefore, it's simply a matter of attempting to calculate the sales potential and/or blockbuster status of pending candidates. Although this is difficult to do with great precision, it can be done accurately enough that a reasonable estimate can be made.

Technological advancements and other scientific breakthroughs can provide a fertile ground of potential business opportunities. The current explosion in “smartphones” and other similar technology devices represent powerful and compelling areas of growth. Of course, the Internet has spawned numerous game changing industries and companies in which to explore. There are many young and very fast-growing companies that have resulted from these breakthroughs that are rapidly becoming household names and concepts. Google (GOOG), Netflix (NFLX), Priceline (PCLN), and many others too numerous to list, are examples of businesses that didn't even exist a decade or two ago. But I caution to not overpay, and to do the work necessary to understand the business to include the competition.

Another example growth industry could be new and dynamic restaurant concepts. Companies like Starbucks (SBUX), Panera Bread Co. (PNRA) and Buffalo Wild Wings (BWLD) are just a sampling of many that have enjoyed recent success. With this type of company, forecasting the future can be as simple as evaluating how many units have penetrated how many markets, and then trying to determine what type of future growth potential remains. The same analysis would apply to companies like Decker’s Outdoor (DECK), Coach (COH), Kohl’s (KSS) and other companies in the retail or luxury goods space. Although I could go on and on, hopefully I have made my point. Forecasting is a process that needs to be approached as comprehensively as possible, but with expectations regarding precision kept within reasonable probabilities.

(Follow this link for a dynamic video of these true growth stocks.)

(Follow this link for a dynamic video of these true growth stocks.)

Challenges and Pitfalls of Forecasting

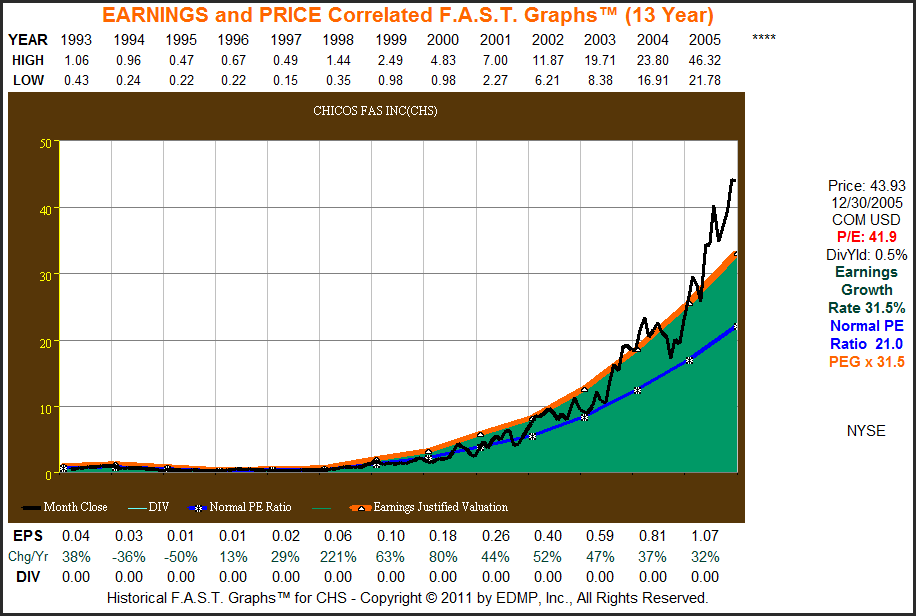

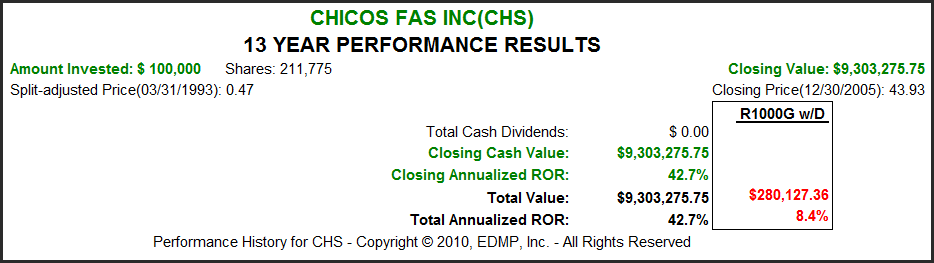

The following example of an extremely successful and fast-growing apparel retailer casts a light on the potential dangers that investors face with growth stocks. The company is Chico's FAS Inc.(CHS), and from the F.A.S.T. Graphs below you can see that this company had an extraordinary record of earnings growth and shareholder results from 1993 to 2005. Price and earnings correlated very nicely; however, by 2005 the company's stock price was overvalued based on my definition of fair value.

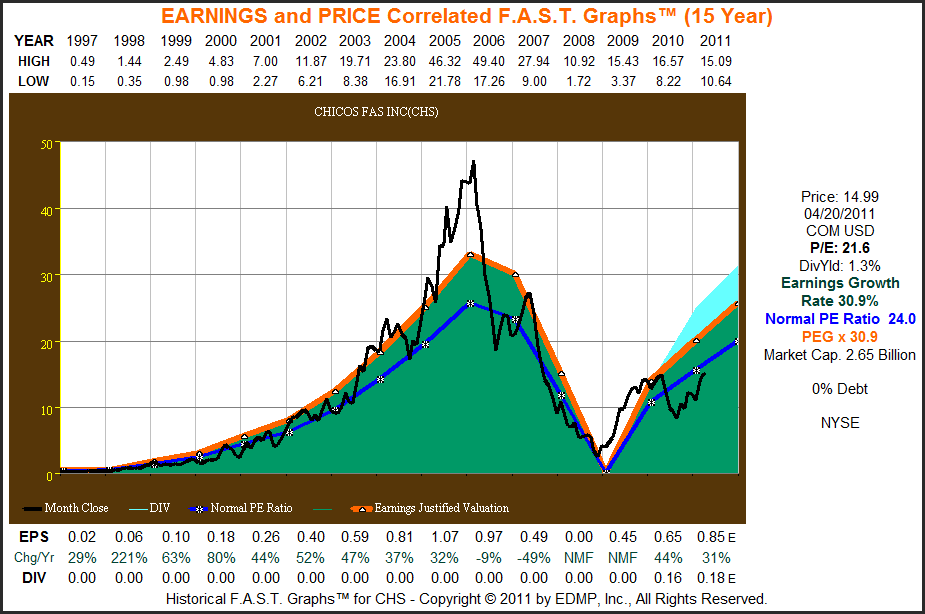

I might add, and be stating the obvious, that this was an extremely popular stock from the late 1990s into calendar year 2005. I would also like to add that expectations for continued growth were also commonly held. However, everything changed abruptly when earnings began to falter in fiscal 2007 (early calendar year 2006). With the graph below we can see the dangers of overvaluation exasperated by the effects of poor business results. As an aside, I can remember being told by many people, including business associates, that I was missing this great company. Fortunately, it was the overvaluation that kept me from owning the stock.

The Power and Protection of Diversification

Throughout this series on “Going for Growth” I have shown numerous examples of true growth stocks that have lavishly rewarded their shareholders. In my last example, Chico's FAS, I showed the potential dangers that can also occur with growth stocks. However, I want to add that because the benefits of owning growth stocks can be so extraordinary when they succeed, I feel strongly that they should not be completely ignored. On the other hand, because they are so rare, I have always believed in owning a portfolio of true growth stocks that was diversified enough to protect capital, but concentrated enough to offer exceptional future returns.

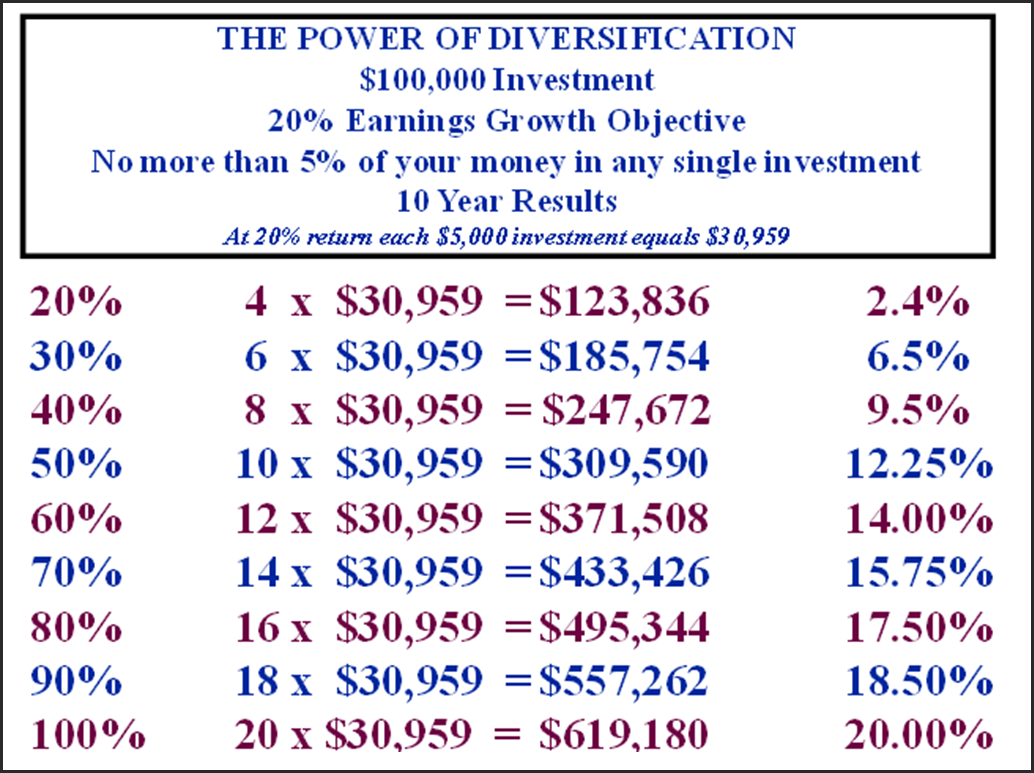

The following chart shows what I call the power and protection of a diversified portfolio of true growth stocks increasing earnings at 20% or above. This is merely a mathematical presentation, and perhaps extreme oversimplification of real world potentials. On the other hand, the math tells a very interesting story. Due to the power of compounding, the true growth stock capable of generating earnings growth of 20% or better can provide an extraordinary rate of return. The chart below shows what would happen at various percentages of success and failure. For example, if only 20%, or 4 companies in the 20 stock portfolio achieved their goals, and the other 16 companies were total failures (prices went to zero) mathematically your portfolio would still achieve a positive, albeit mediocre rate of return.

On the other hand, if only half of your companies succeeded (50%) and the other half failed, your long term return would still be exceptional. In the real world, events would probably never happen like the chart depicts. Even the Chico's example above did not go to zero. What the math is really telling us is how powerful just getting a few true growth stocks right can be.

Conclusions

As I have attempted to illustrate with this three-part series on “Going for Growth”, the rewards for investing in this equity class can be quite substantial and exciting. Conversely, the risks of investing in this equity class can also be high and/or severe. But most importantly, I hope I have shown that there are sensible and prudent ways to participate in this dynamic category while simultaneously mitigating risks to reasonable levels. This asset class is not for everybody, and does require a great deal of diligent monitoring. There are no shortcuts or easy methods, in my opinion.

I also believe that the same can be said of investing in any asset class, to include blue-chip dividend growth stocks. One of the things that attract many investors to the dividend category is the consistency and persistence of their historical records of both earnings growth and dividend growth (Dividend Champions, Aristocrats, etc.). This is the same concept that has attracted me to the true high-growth stock category. This is why I have always included a few blue-chip moderate dividend paying growth stocks within my portfolio of more aggressive true growth stocks. Total return and the power of compounding are important concepts that I believe every investor should consider and understand. Finally, note the stocks in this series are offered as recommendations to buy or sell. As I've already stated, I leave that decision to the discretion of each individual investor.

No comments:

Post a Comment