Portrait of a Beautiful Dividend Growth Stock - Seeking Alpha

I don’t know why I remember this, but when I was a kid, I found a movie magazine in my grandmother’s house. It had an article that tried to describe the ideal movie star’s face (female persuasion). So they took, like, Marilyn Monroe’s mouth, Jane Russell’s eyes, and the chin, cheekbones, forehead, and hair from other actresses they considered to be best of type. Using the cut-and-paste technology of the times, they glued together pieces of pictures to create the ideal actress’s face.

The result was a mess. Even to my young eyes, what they wound up with needed some work, shall we say. The lesson to me was that it’s as much about how things fit together, not just the beauty of the individual pieces, that creates a beautiful face.

I think the same principle applies to companies and their stocks. The best dividend-growth stocks come in all shapes, sizes, industries, and so on. It’s how management puts the pieces together over a long period of time, plus how the market values the stocks, that determines whether we have a beautiful dividend-growth stock.

While I may be repeating the same mistake of that magazine, I am going to try to create a portrait of a beautiful dividend-growth stock. This portrait will reflect some biases that I have:

- A minimum 3% yield, or 2.5% for stocks that have raised their dividends for at least 20 straight years.

- An ironclad requirement that I understand how the company makes money, what its business model is, and that management is committed to dividend growth based on all the evidence I can find.

- At least five straight years of increasing dividends.

- No tobacco stocks (for personal reasons).

- A five-year total return that has at least kept pace with the market

I have now published four annual Best Dividend Growth Stocks e-books. Twelve stocks have made the Top 40 list every year. I will use 10 of those 12 as my “beautiful faces” to grab parts from. (I dropped one REIT and one MLP because of valuation and taxation issues. That skews the yields lower, but it means that the remaining 10 companies are all organized as conventional corporations.)

At the risk of putting a dent in future sales of my e-book, here are the 10 “all stars” that have made the Top 40 every year:

- Abbott Laboratories (ABT)

- Chevron (CVX)

- Chubb (CB)

- Coca-Cola (KO)

- Johnson & Johnson (JNJ)

- McDonald’s (MCD)

- PepsiCo (PEP)

- Procter & Gamble (PG)

- 3M (MMM)

- V.F. Corp. (VFC)

Many other worthy stocks have made at least one Top 40 over the years. Several have made it two or three times. But these 10 have managed to make the Top 40 every year. Based on the scoring system that I use, they have scored the highest, year-in and year-out, to beat hundreds of candidates every year.

Among other things, that means they have been fairly (or favorably) valued at the beginning of each year. Overvaluation is one reason that an excellent dividend company can fail to make the Top 40 in a particular year. Indeed, some of these companies (JNJ comes to mind) would not have made it 10-12 years ago; they were way overvalued and their yields were simply too low. That’s one way that market forces come into play even in a long-term “market-agnostic” strategy such as investing for dividend growth. The fact is that you need decent valuations to produce decent yields.

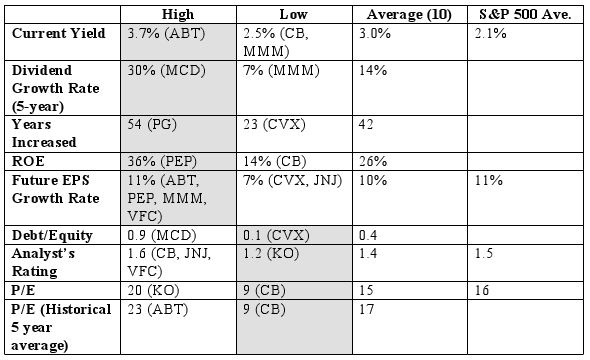

Okay, here’s my effort to construct the ideal face of a beautiful dividend-growth stock. For the mouth, eyes, etc., I have used some of the >20 metrics that I use in ranking dividend-growth stocks. The shaded cells represent the most beautiful face. The all-star average is presented along with S&P 500 norms where available from Morningstar. (Stock data was collected in early January; S&P data was collected on 3/23.)

The most beautiful dividend-growth stock would have the attributes that are shaded. Of course, you could think up even better attributes in theory. But, like the beautiful Hollywood faces, what we have here are attributes of real stocks, not theoretical CGI avatars.

I’ll make a few observations. Some of the following are in anticipation of questions and objections that are likely to surface in the comments.

- The yields are too low. These are dividend-growth stocks, not the highest-yielding stocks. As much weight has been placed on the reliability of annual dividend growth as on yield and yield growth. Actually, the 3.7% “beautiful” yield falls near the high end of what some dividend-growth investors consider to be the “sweet spot” of the best dividend-growth stocks.

- Where’s Altria (MO)? I recognize that MO is a terrific dividend-growth stock. But I don’t invest in tobacco companies for personal reasons (smoking killed both of my parents). This is not an ethical position that I force on other people; it is simply my practice.

- Debt ratios are low. This makes sense. A high-debt capital structure is a frictional cost for any company. A few companies make it work for many years. When it works, it’s called leverage. When it doesn’t work, it’s called risky or stupid. But it is not surprising that the most consistent and successful dividend growth companies tend to operate with low debt.

- Dividend growth rates are healthy. The most beautiful “face” has a 30% five-year DGR, and the average of all 10 is 14% per year. Those kinds of growth rates will keep you comfortably ahead of inflation.

- ROEs are high. There are various measures of management effectiveness. ROE is the one that I use. It’s not surprising that ROEs would be healthy in the highest-rated companies. It’s especially impressive when a company can achieve a high ROE with modest debt. Seven of the 10 companies have had ROEs greater than 15% for at least five straight years, and another is on a four-year streak.

- Future EPS growth rates are not very high. Ideally, I’d like to see higher EPS growth rates. But these are real dividend-paying companies, not theoretical ones. Every one of these companies is well established. Each has long since reached a point in its corporate life that its annual EPS growth rate has left the stratosphere and settled in at a moderate, sustainable rate.

- "I can’t believe you use analyst ratings in your analysis." From the beginning of my financial writing, I vowed to use only data that is available free — that’s the most accessible to individual investors. It’s true that analyst ratings are often overblown. So I scale them back. There is still a correlation, I have found, between analyst ratings and stock performance. On the common scale of 1 = Strong Buy and 5 = Sell, these stocks rank well. Note that lower is better on this scale, like golf. I realize that many investors use paid services such as Value Line or Morningstar Premium. However you do it, I think it’s good to get third-party opinions into the mix when you are evaluating stocks. You can discount them for biases.

- P/E ratios seem about average. One often associates “boring” dividend-growth companies (or sectors, like utilities) with low P/E ratios. My experience is that the best companies don’t usually come exceedingly cheap. Perhaps the market recognizes the inherent value in a reliable future dividend stream just as much as the potential for capital gains.

Well what do you think? Is that a beautiful face, or what?

Disclosure: I am long ABT, CVX, CB, JNJ, MCD, PEP, PG, MMM.

No comments:

Post a Comment