ScotiaBank: The Most International of Canadian Banks Looks Attractive

I guess you already know my love for Canadian Banks by now. The Big 6 (Royal Bank (RY), TD Bank (TD), ScotiaBank (BNS), CIBC (CM), Bank of Montreal (BMO) and National Bank (NTIOF.PK) are solid companies evolving in a sector that is both solid and is heavily protected by the government; Canadian financial institutions. To be honest, I think that if you buy any Canadian Bank, you are making a good deal. In this dividend stock analysis, I’ll tell you why BNS is my pick.

Company Stock Description

ScotiaBank is the 3rd largest bank in Canada in terms of assets. One thing I really like about it is that while they are pretty strong in Canada, they are also the most international of Canadian Banks. They have over 70,000 employees working in more than 50 countries. Besides their Canadian activities, they are mainly active in South America and Asia. With all those countries, it’s better than currency trading! BNS offers everything a bank can offer through their divisions (savings and loans, investing services, trust, commercial banking, wealth management, international financial services, etc.).

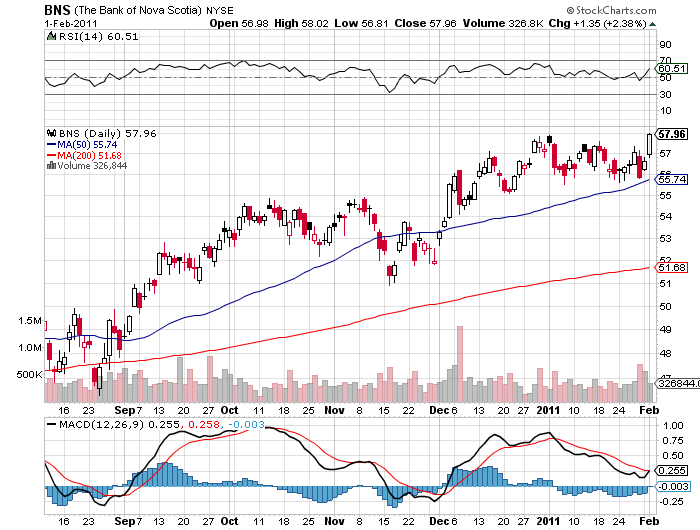

Stock Graph

Click to enlarge

Company Ratios and Financial Info

Dividend Metrics (as of Jan 2011):

- Current Dividend Yield: 3.50%

- 5 year Dividend Growth: 7.58%

- 1 year Dividend Growth : 0%

Company Metrics:

- Sales Growth: 5.67%

- Earning Growth: 33.04%

- P/E Ratio: 14.41

- Margin Growth: N/A

- Payout Ratio: 50.1%

- Return on Equity: 18.06%

- Debt to Capital Ratio: 1.20

Stock Metrics:

- Ticker: BNS (on TSE (Canadian) and on NSE (US))

- Price: $56.46

- Trading Volume: 3,232,840

- Trend (technical analysis): Trading over moving average

Upcoming opportunities and dangers

BNS is clearly capitalizing on one of their main advantages; they grew stronger from the 2008 credit crunch. All Canadian banks kept posting profits and increased their capital. This is how ScotiaBank recently bought DundeeWealth (Canadian wealth Management Company) in order to increase its presence in the wealth management sub-sector. This allowed BNS to jump from the 11th to 5th place in terms of assets under management in Canada.

Another great point is that financial analysts expect BNS to raise their dividend in 2011 (going back to a raise every 2 quarters scenario). This is always good news for dividend investors.

On the other hand, while BNS takes care of its Achilles’ heel in wealth management, it will certainly not be the leader in term of loans in Canada. In fact, their growth will definitely not come from this sector which is led by other Canadian Banks.

While I like the fact that BNS is diversified among many South American and Asian countries, this also exposes them to more economic fluctuations in those countries. A double-dip recession in some countries will affect them badly.

Final Thoughts

Since I am already holding the smallest and most Canadian concentrated bank in my portfolio (National Bank, NA), I think that BNS will be a great addition to my portfolio since it is completely the opposite. I certainly don’t expect the stock to rise like there is no tomorrow (this chance happened in 2009… now it’s too late). However, I think BNS will be a solid dividend payer that will raise its dividend from time to time.

I should be getting an additional $5,000 in my brokerage account by next week. BNS will definitely be a buy at that time.

Disclosure: Author holds National Bank.

Thanks Dividend Guy for the review of BNS. The p/e of 14.41 might be justified on the growth rate of earnings, but the 0% 1 year dividend growth rate + the 3.5% yield do not justify it. Price growth since 2008 has been flat after the recovery from the Great Recession.

Molaski - 40 years saving is an amazing accomplishment, congratulations! Just curious about your comment, "Monthly Dividend stocks are the way to go because thats the way to grow." BNS pays dividends quarterly, are you saying that you prefer monthly investments as opposed to BNS?

tweedn - txwoodworker is correct, "The flat dividend growth rate was imposed by the government. It does not reflect the bank's underlying ability to pay dividends and grow them." BNS is currently the most international of the Canadian Big 6, and it has used this year to expand it's business reach and operational capacity. Looking forward, BNS is positioning itself to be a very respectable international financial institution.

Personally I am looking for a dip to initiate a position, however, looking forward 5-10 years, long after the divi has been reinstated BNS will be trading along side TD in the $80-$100/share range, and for good reason....IMO.