McDonald's: A Fairly Valued Dividend Champion

article to

Like any disciplined long term investor, I have a ‘wish list’ of stocks that I purchase on pullbacks. For me, McDonald's (MCD) has always been one of those companies. Not only is the food cheap and delicious, the stock is fairly valued and yielding a substantial dividend. Plus I’m an American. It’s engrained in our DNA to eat Big Macs.

Whether you like it or not, McDonald’s hamburgers are as American as apple pie (which coincidentally you can get from its dollar menu). I know there are headwinds to the company, the health risks, rising input costs, market saturation, bad publicity, etc. Heck, even I saw Super Size Me.I’ll admit that guy put on a little weight, but he looked healthy enough… in that 17th century European Royalty sort of way.

Hey, any press is good press. But no matter how you feel about the golden arches, McDonald's possesses one of the strongest brand equities of any company worldwide and will continue to expand its empire into emerging markets.

What It Does:

Just in case you live in a cave, McDonald’s sells cheeseburgers, chicken products, French fries, breakfast items, soft drinks, shakes, coffee and desserts. It also derives a considerable amount of revenue from the rent of its properties to franchisers. But mostly, it provides double cheeseburgers for my family on road trips.

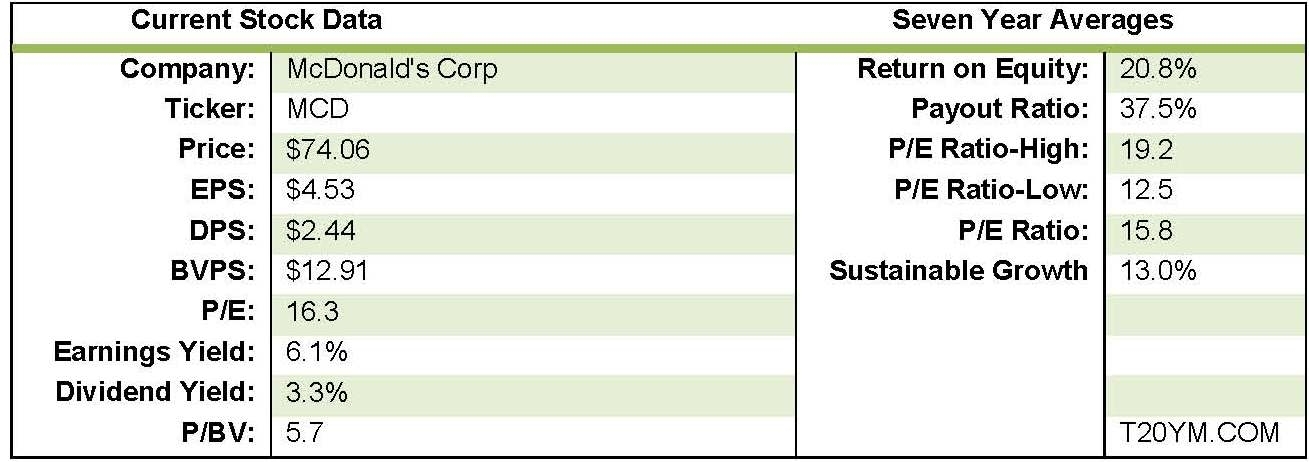

The Fundamentals:

click to enlarge images

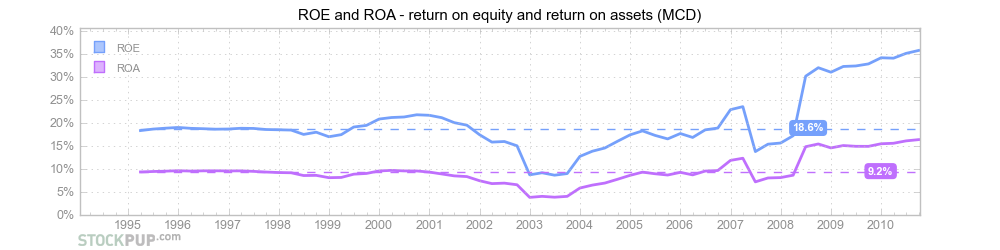

Fundamentally, MCD is a sound stable investment. It has provided its share holders with an impressive 21% return on equity over the last 7 years, and a ROE of 18% for the past 15. The average ROE for American companies over the same time period was 12% making MCD’s ROE of 21% very attractive.

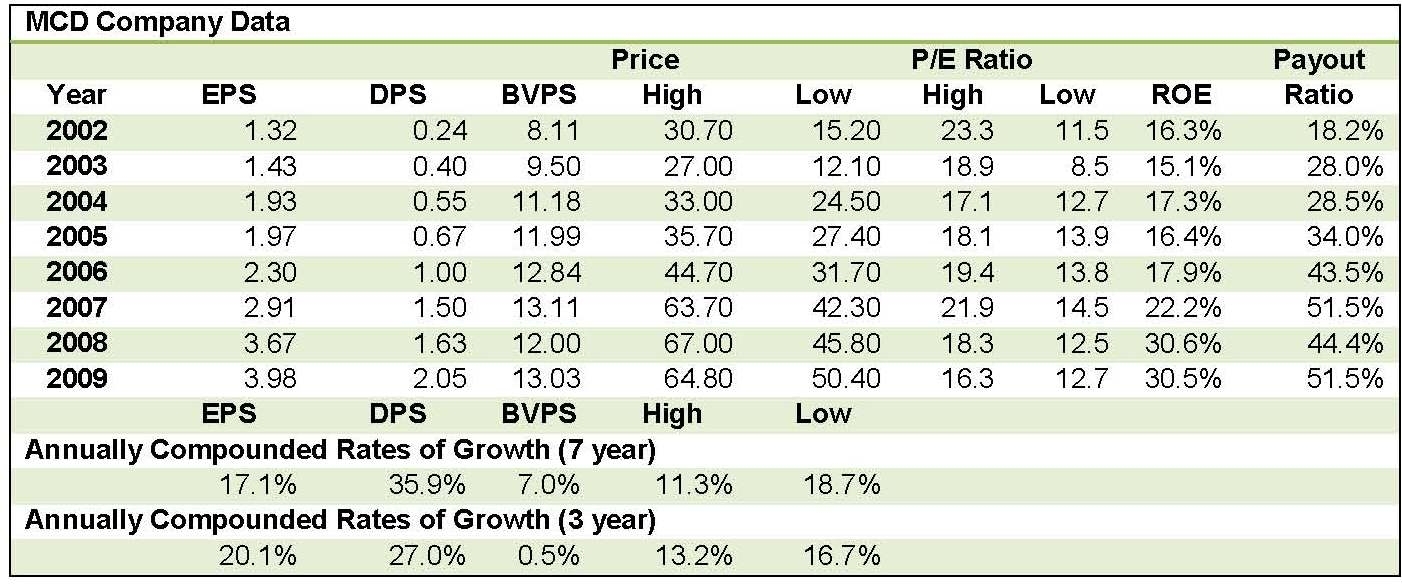

Furthermore, MCD has grown its earning per share consistently for the last 7 years, offering its investors a 17% annual compound growth rate over the time span. Considering the severity of the economic downturn felt in 08-09, this is a very commendable achievement.

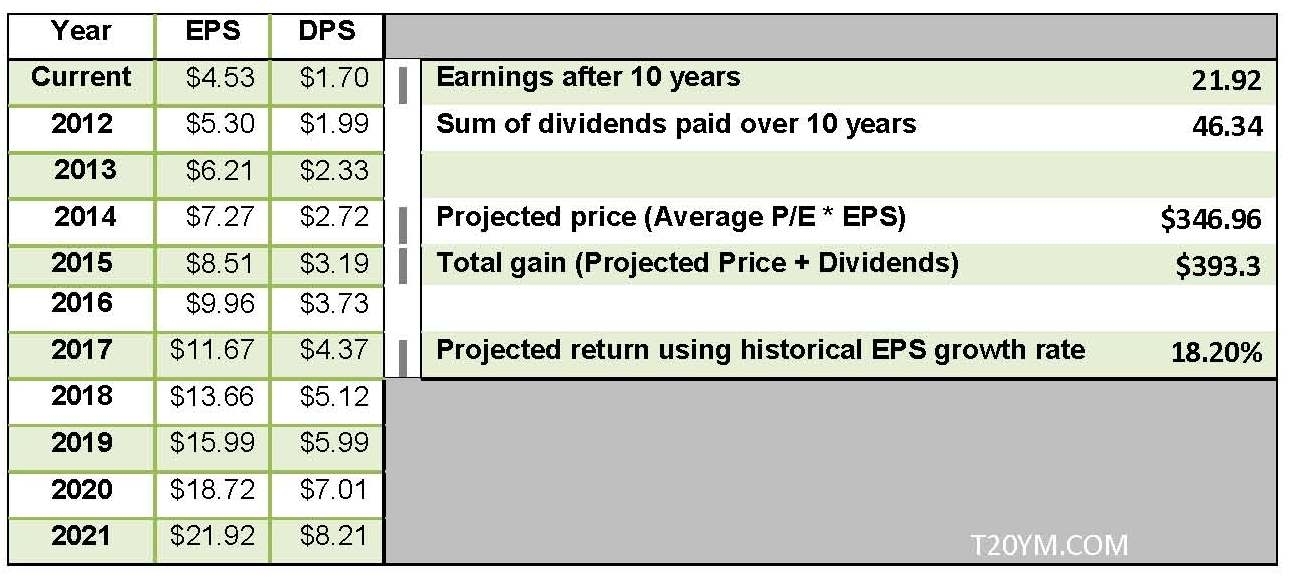

When we take MCD's past compound growth rate and model the company’s future EPS using these ratios, the results are staggering:

Obviously, these valuations are lofty, but still attainable. At some point, market saturation will become a legitimate headwind for the company. You can only have so many McDonald's in Tunisia. But one of the greatest growth markets for American companies is barely tapped. Even though MCD generates 75% of its revenue internationally, it only operates 1100 restaurants in mainland China.

McDonald's’ opportunity for growth in China is incredible. Additionally, the Wall Street Journal predicts that McDonald's plans on doubling its presence in China by 2013. Nothing in the company’s history makes me doubt this statement. MCD is a model of consistency, growing earnings regardless of economic conditions.

Returning Value to Shareholders:

For long term investors, companies that pay sustainable dividends are very important. McDonald's offers investors one of the safest, fastest growing dividends in the DJIA. In fact, McDonald's is part of the elite Dividend Champions Club. It has raised its dividend payment for 37 years straight. Currently McDonald's is yielding 3.3% with a payout ratio of 49%. The payout ratio is inching close to the 55% mark where I generally start to get worried about sustainability. However, MCD seems to have found the niche where it can expand it business while consistently rewarding its shareholders with dividend payments.

McDonald's has also increased shareholder equity through share repurchases. Over the past 4 years MCD has repurchased nearly 14 billion dollars worth of shares. These repurchases have reduced the float of MCD shares on the open market by nearly 25% raising the value of the common stock.

click to enlarge images

Between its lofty dividend and its share repurchases, McDonald's has shown a firm commitment to returning capital to its shareholders.

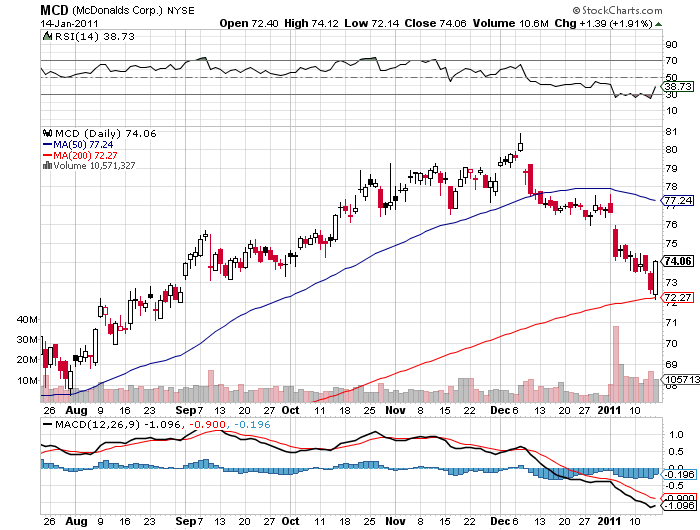

The Technical:

For long term investors, talking charts is a faux pas. It’s like discussing feet with Rex Ryan at the dinner table. I agree that for long term holders, fundamentals matter more than a bar chart. Nevertheless, technical analysis is another tool in our utility belt. It would be foolish not to utilize it. Saving a few dollars on an entry point will add up, especially when those savings are compounded over an investor’s lifetime. Take a look at the MCD chart for the last 6 months:

From August to November, this was a chart of astonishing beauty. It showed lower lows, higher highs, basing patterns with solid break outs. Then, around December 8th, something went horribly, horribly wrong. MCD gapped down, then continued to move lower with increasing volume. What set off this tremendous selloff? Was Ronald McDonald caught defecating in the ball pit? Was MCD linked to GS or BP? Did people finally realize the Mcrib is the most disgusting sandwich since the D'angelos Lobster Rolls? No, nothing this exciting. McDonald's' November global sales simply rose 4.8%, narrowly missing the streets estimates. The stock began to sell off. Then it sold some more. Then, on January 4th, it sold off 2% on ridiculous volume crashing through key resistance levels in the process. Sometimes the market just doesn’t think. It just sells.

Luckily the market eventually corrects. As you can see from the chart above, MCD made a strong push on Friday as it bounced off its 200 day moving average. I believe this high volume reversal is a great entry point for MCD. The RSI says oversold and the MACD is heading north. A 10% sell off in a stock I love is a buying opportunity. Nothing has changed fundamentally, just some yearend profit taking, and readjusting of portfolios.

Overview:

McDonald's is large cap global company. It is one of the most iconic brands in the world today. Its management provide above average ROE for its shareholders. Additionally, the headwinds that the company faces cannot stop its momentum. It is fairly valued with a forward P/E of 14.4, falling in the middle of its historic range. MCD’s dividend yield is strong, stable, and growing. It remains one of my top holdings that I will continue to add to on weakness. Its current pullback is an excellent entry point for new investors. I view MCD as a long term buy and hold stock. I’m off to get a Big Mac meal, super sized with a diet coke.

Disclosure: I am long MCD.

No comments:

Post a Comment