The Intel Transformation: From Growth Stock to Value Stock

This article isn't about the transformation of Intel (INTC) from a PC chip company to a diversified chip manufacturer involving smartphones and tablets. Rather, it is to offer what I believe is a primary reason why the stock price has languished for years despite record-breaking earnings, solid revenue growth, strong cash flows, increasing dividends, and consistent, if not flashy, future business projections: The stock is transforming from a growth stock to a value stock.

Intel shares have been wandering the wilderness for years. In October, Iwrote an SA article that outlined how Intel shares were being treated more like those of a utility stock than technology shares. The premise has not changed much. As of December 31, the iShares Utility ETF (IDU) had a trailing PE ratio of 15X and sports a yield of 4 percent. The fund has risen about 1.6 percent to-date. Intel closed last Friday with a multiple of 10X and a 3.4 dividend yield. The shares have risen 0.2 percent to-date. Indeed, INTC is being viewed as having somewhat less future growth prospects than a utility company. The dividend yield is competitive with many utilities and the dividend growth rate is superior.

The transformation from a growth stock to a value stock can be a long and arduous haul. As growth investors move away from a stock, the share price drifts nowhere. Selling begets more selling and investor disappointment creates a self-fulfilling prophecy. Nearly all of the company news is interpreted in a negative light. The PE multiple is driven down. Large institutional "growth" investors cash out, not to return. Eventually, the value investors begin to move in, seeking a "bargain." Their screens look for equities with low multiples, consistent cash flow, dividend yield / growth, and demonstrated earnings stability.

Sounds familiar? Intel stock has spent the better part of the past seven years wandering, in a sort of equity twilight. Share prices topped out as a growth play in 2003 and 2004. The transition from a growth to a value stock began in 2005 and meandered into 2007. Cash flows and EPS essentially flattened out, aimless from 2004 through 2007. Nonetheless, the levels at which these figures meandered remained consistently strong: During this same time period, cash flow per share remained in the $2 range. Meanwhile, the dividend tripled.

The transformation process was put on hold during the Great Recession and associated stock market meltdown of 2008 and 2009. Indeed, as is often the case with stocks, Intel's situation was not catagoric, but contained a subplot. While transforming from a growth to value play, the shares also retained elements of a cyclical tech stock. Therefore, the recession put a double-whammy on the company: While in the midst of a growth/value transition, the stock got pounded when the economy went into a free fall. Finally, beginning in late 2009 and into 2011, the consistent signs and signals of a value stock are being reinforced.

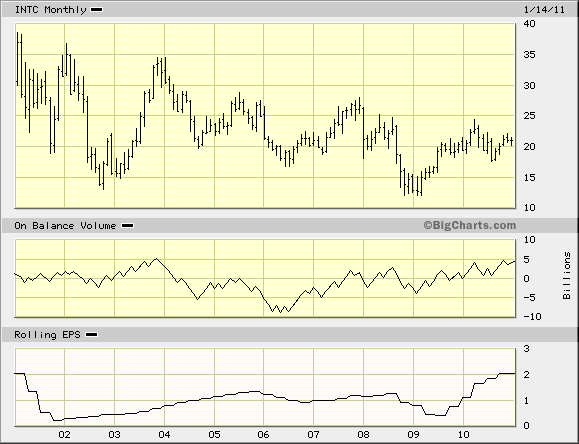

In addition to the fundamentals falling into place, the technical charts offer some confirmation. Below is the ten-year monthly chart. Note the on-balance volume trending up and breaking the zero line since 2009, suggesting that the big players are noticing, despite the share stagnacy. EPS, also shown on the chart, has likewise ramped up.

INTEL TEN-YEAR MONTHLY CHART

Bottom line: I envision Intel attaining recognition as a value play in 2011. Large investors will find the PE multiple, cash flows, yield and dividend growth rate attractive. I forecast earnings over the next two years in the $2.25 to $2.45 range. Placing a 12X-13X multiple on the EPS translates into a share price between $25 and $32 a share, depending upon how bullish one forecasts. Starting at $21, and including dividends (which have now increased eight years in a row), that's a decent return for the patient investor.

Disclosure: I am long INTC.

No comments:

Post a Comment