In part 1 we talked about how and why we are currently avoiding bonds altogether. We understand that this is a radical viewpoint, and that diehard asset allocation advocates will vehemently disagree. However, we are comfortable with our position because we believe that the traditional safety profile offered by bonds does not exist at today's extremely low interest rate levels. Furthermore, we believe that bonds need to be long-term investments in order to reap the safety profile that they offer.

The general ideas behind a bond are a fixed interest rate payment (coupon) and a 100% return of capital at maturity. In other words, we believe that bonds should be bought and held to maturity if safety is the driving force behind owning them. On the other hand, it is a fact that bonds, like stocks, do trade daily. However, we have never been an advocate of trading bonds because of their limited upside potential. While common stocks, at least in theory, have no limit to how high they can go, bonds are restrained because of their ultimate movement back to par.

If interest rates drop after a bond is issued, its price will go to a premium, but once again, within limits. We have never seen a bond priced at three or four times its par value. We have seen bonds trade at a 30% to 40% premium to their issuing price, but rarely higher than that. Of course the only way to capture the premium is to sell the bond. Because, as the bond gets closer to maturity, its value will go back to par (original issuing value), therefore, any premium return will eventually dissipate. So, even though a bond’s coupon never changes once the bond is issued, its price can be very volatile.

The following graphic on the historical rates paid by 10-year Treasury notes since 1962, courtesy of Yahoo Finance, vividly illustrates how extremely low interest rates actually are today. Also, notice that even though the long-term trend since the early 1980s has been descending downward, there have been periods of rising interest rates in between. In other words, interest rates, like stock prices, never move in a straight line.

(Click to enlarge)

A Summary of the Current Risk with Bonds

Since safety is theoretically the major redeeming quality of a fixed income instrument like a bond, this series of articles has focused solely on treasuries. It's a given that the Treasury Bond will return the investor’s principal at maturity. However, if the risk profile on the safest of all bonds is higher than ever, one can only imagine what has happened to the risk profile of all other classes of bonds. The point we are trying to make is that bonds are moving closer to the risk profile of stocks, but without offering the potential higher reward of stocks.

At the risk of stating the obvious, there are several problems in addition to a potential drop in the price of the 10-year Treasury Bond when the yield is below 3%. When inflation rears its ugly head, and we believe it eventually will, an already inadequate 3% yield could easily go to zero, because of loss of purchasing power. Consequently, it is at least theoretically possible that cash is the better option if you're that frightened. With cash, only your purchasing power will fall at the rate of inflation, but the nominal value will remain the same.

The only way to get a better yield is to go to longer maturities than 10 years, which only exasperates the risk by locking in a low yield for a longer period of time. The 30-year Treasury Bond is only offering a yield slightly above 4%. Consequently, when interest rates do go back to more normal levels, you're stuck with essentially illiquid paper that is paying a low return. Bonds would typically offer higher income and more stable values (lower volatility) than stocks, but the risk is high that this may not be true for at least the intermediate future.

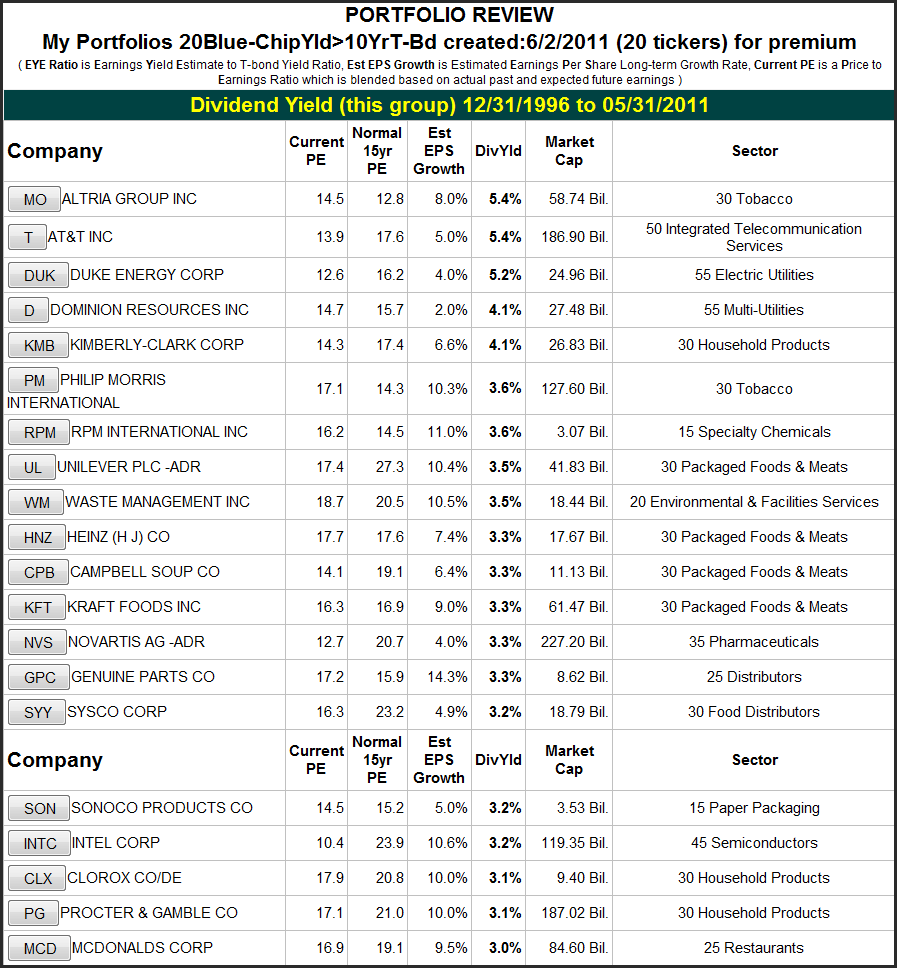

20 Blue-chip Dividend Growth Stocks with Yields Higher than the 10-year Treasury Bond

The following portfolio review lists 20 blue-chip dividend paying growth stocks with dividend yields in excess of a 10-year Treasury Bond. Although not all on this list are Dividend Champions or Dividend Aristocrats, most have a history of offering some dividend growth and capital appreciation potential. Importantly, this is only a sampling of many more names that could have been listed. On the other hand, readers should be aware that it is quite remarkable to be able to show this many quality names that pay dividends greater than a 10-year Treasury Bond.

(Click to enlarge)

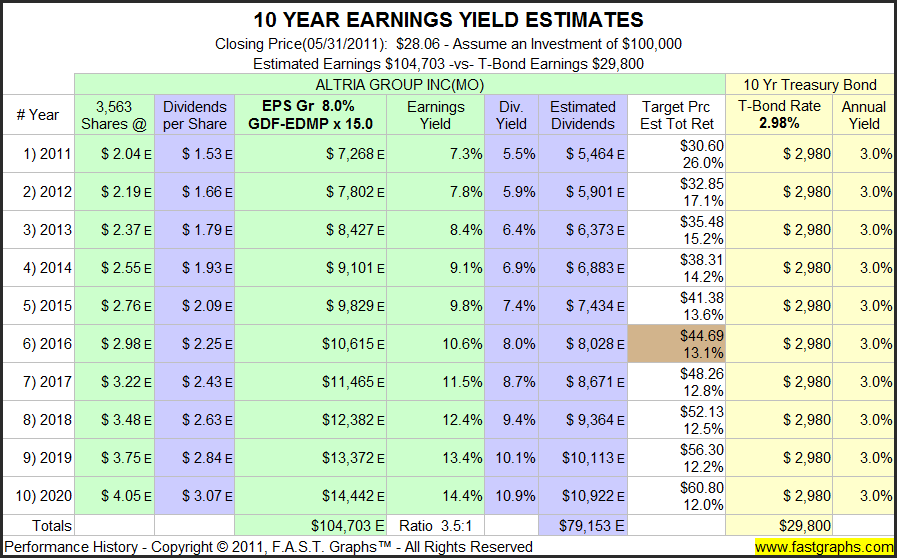

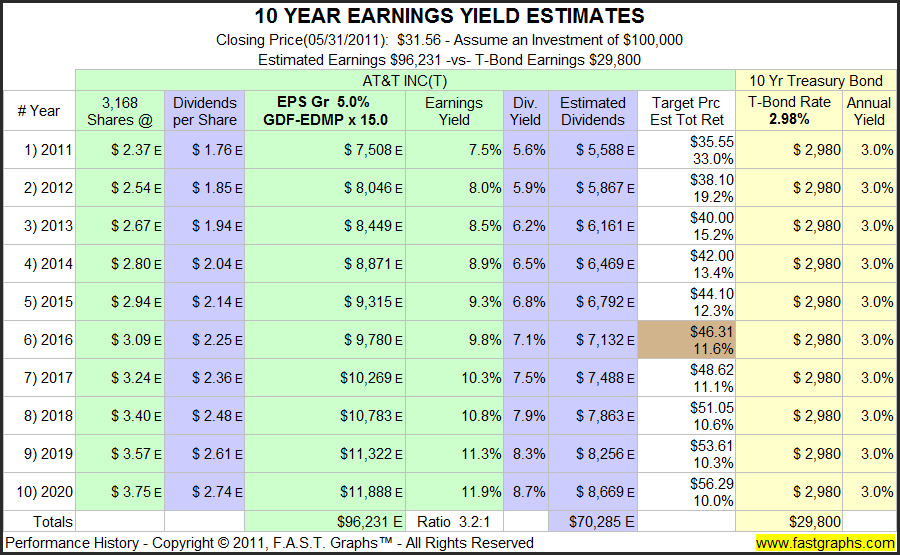

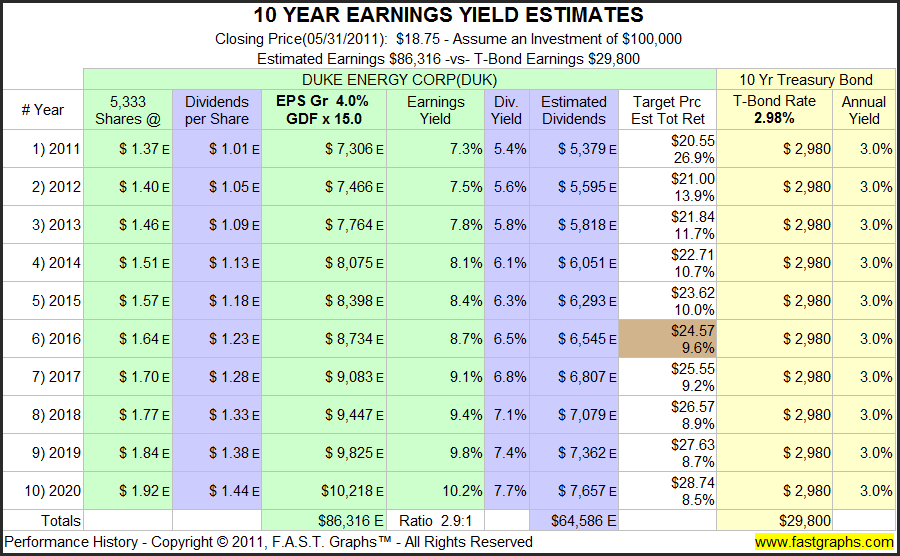

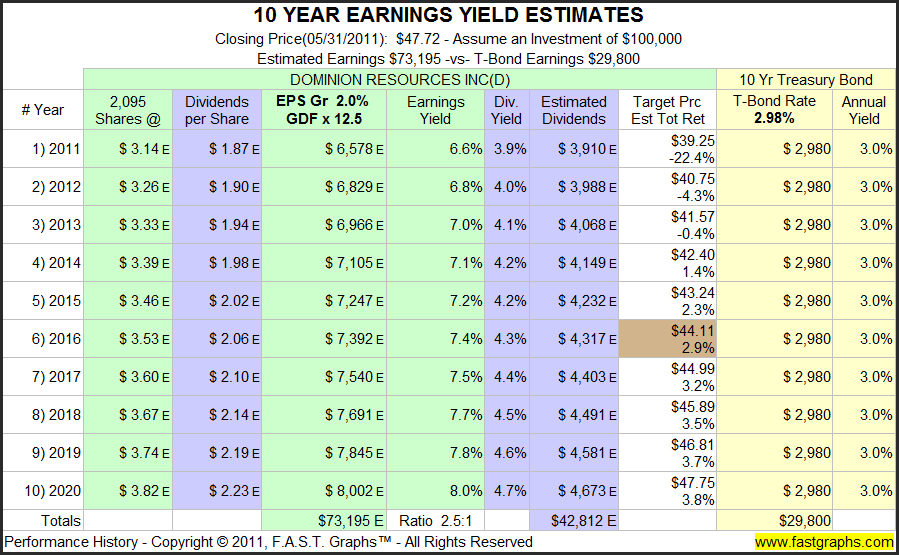

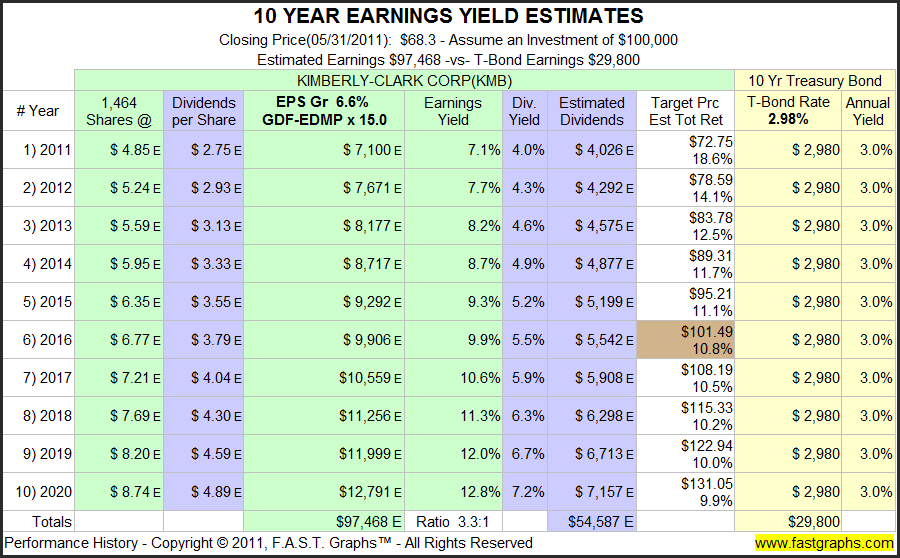

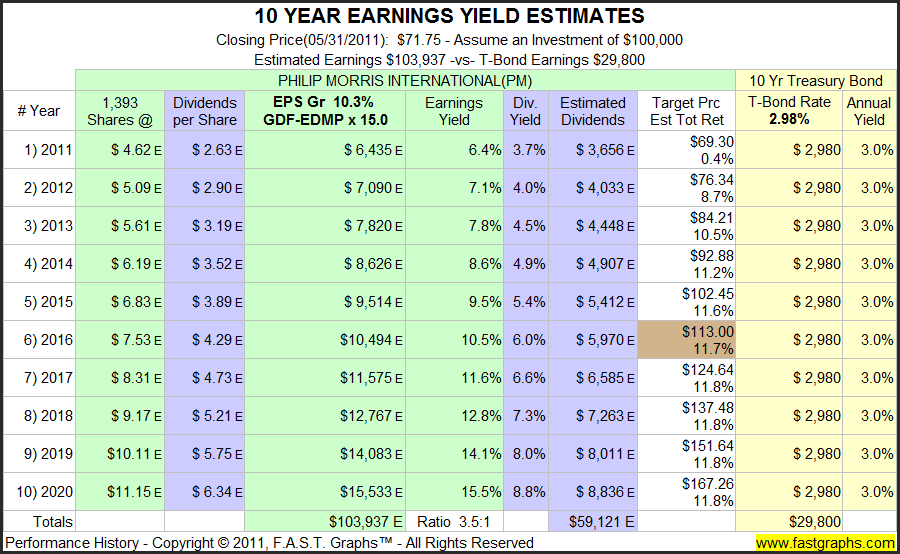

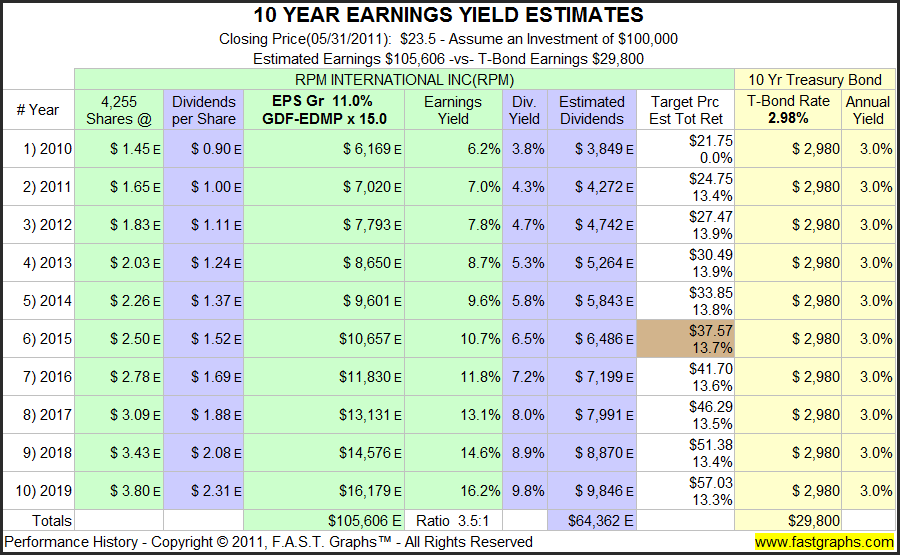

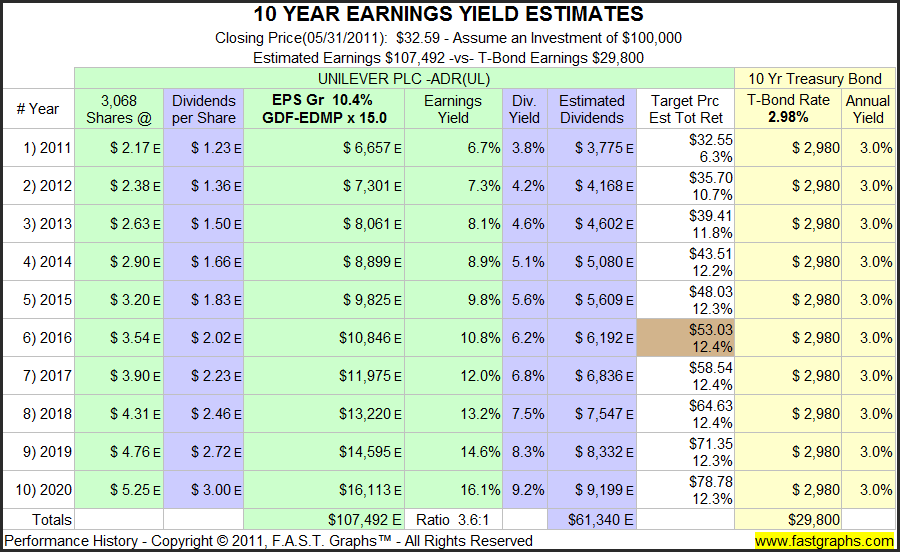

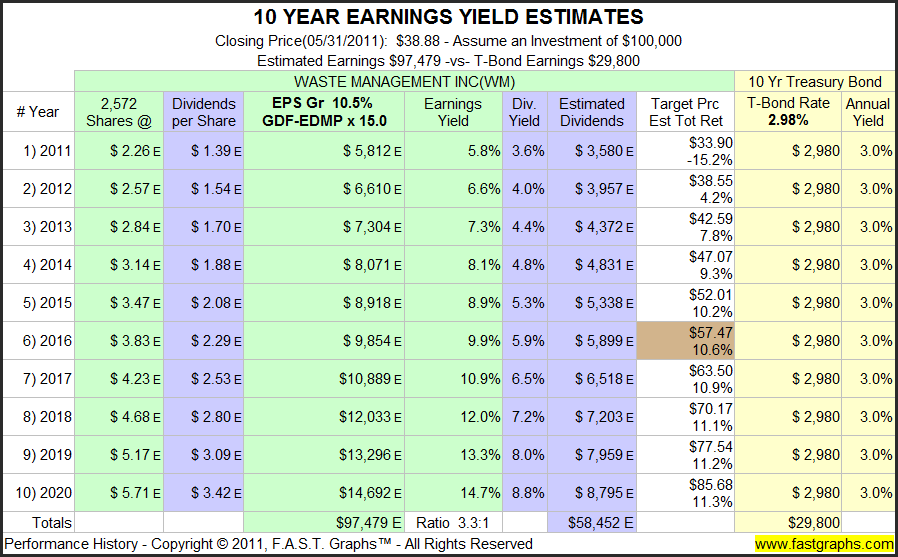

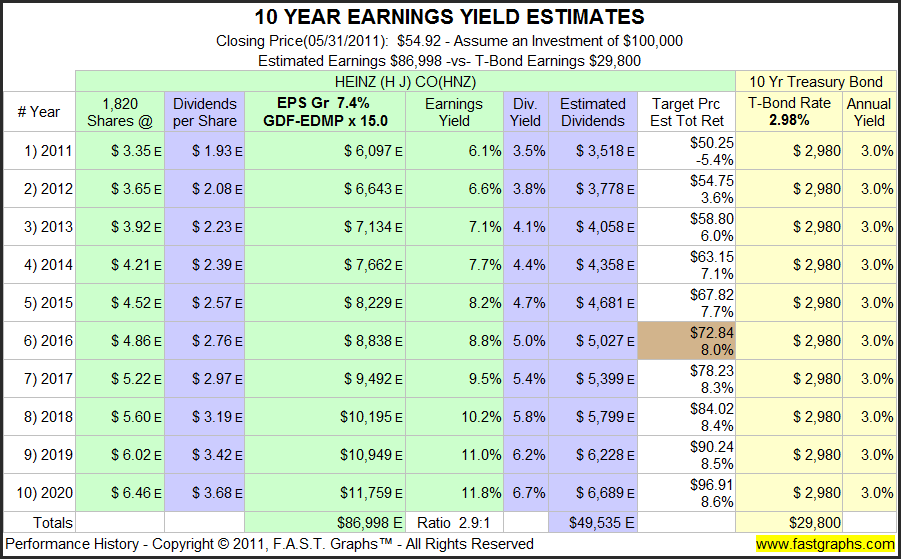

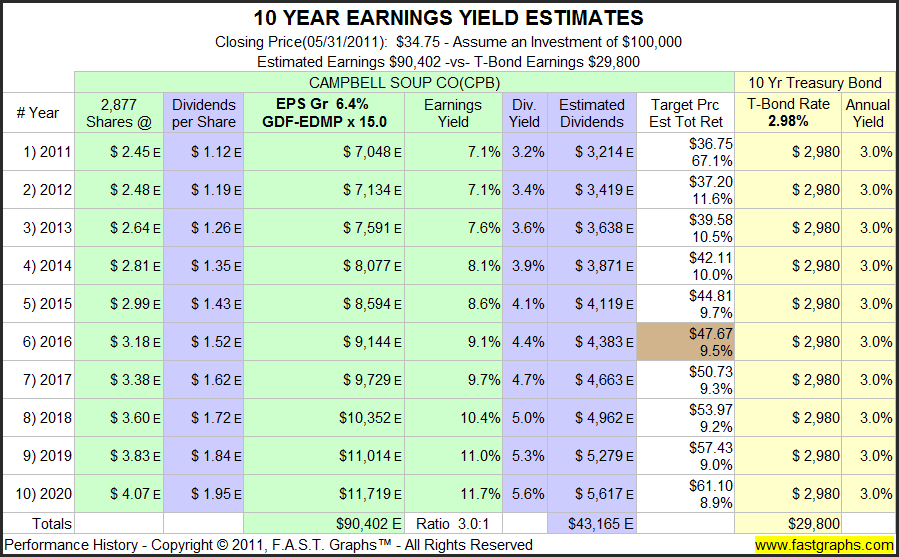

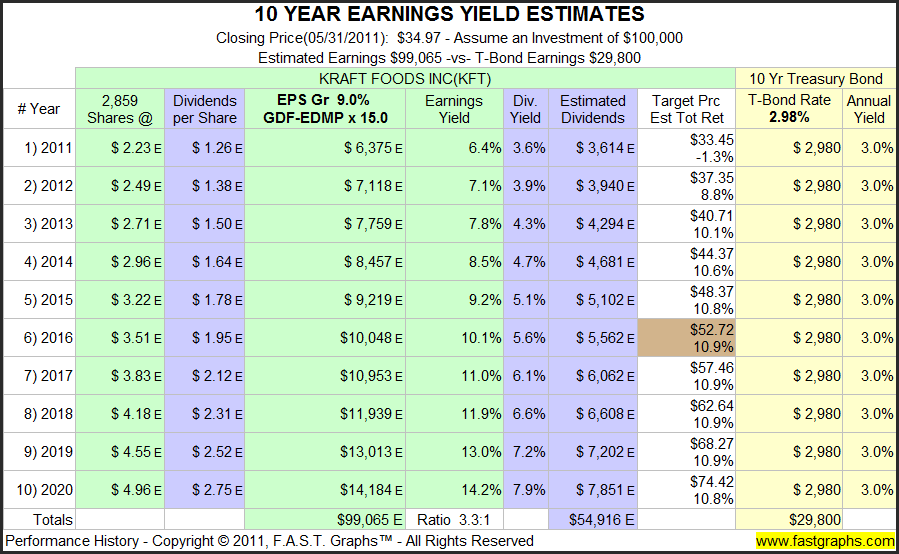

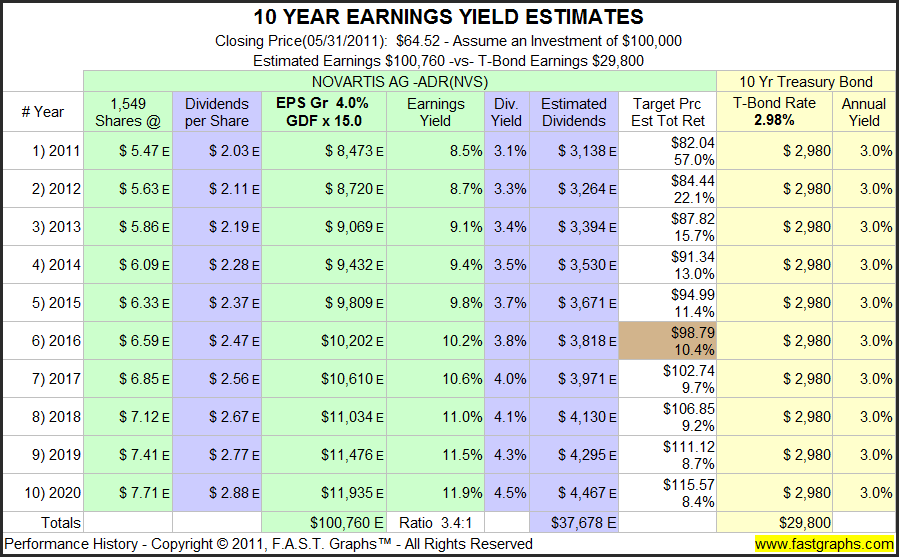

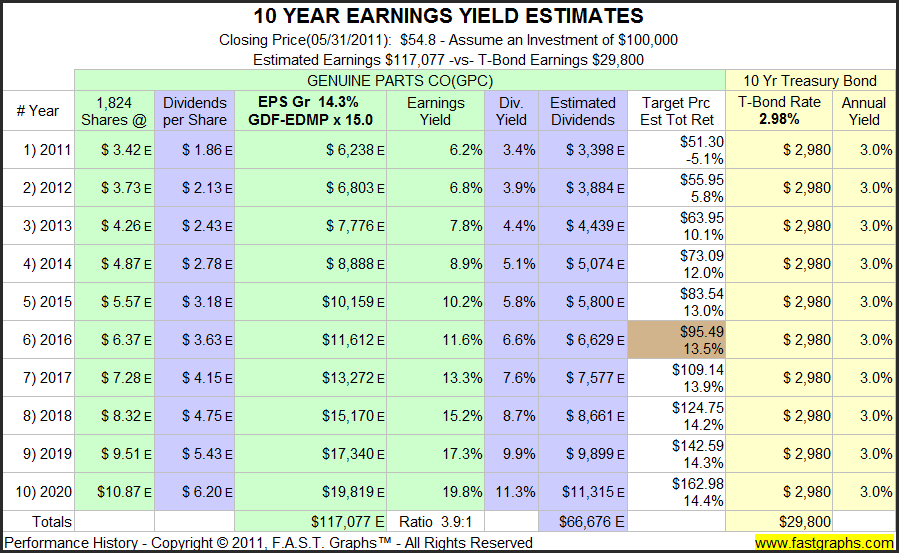

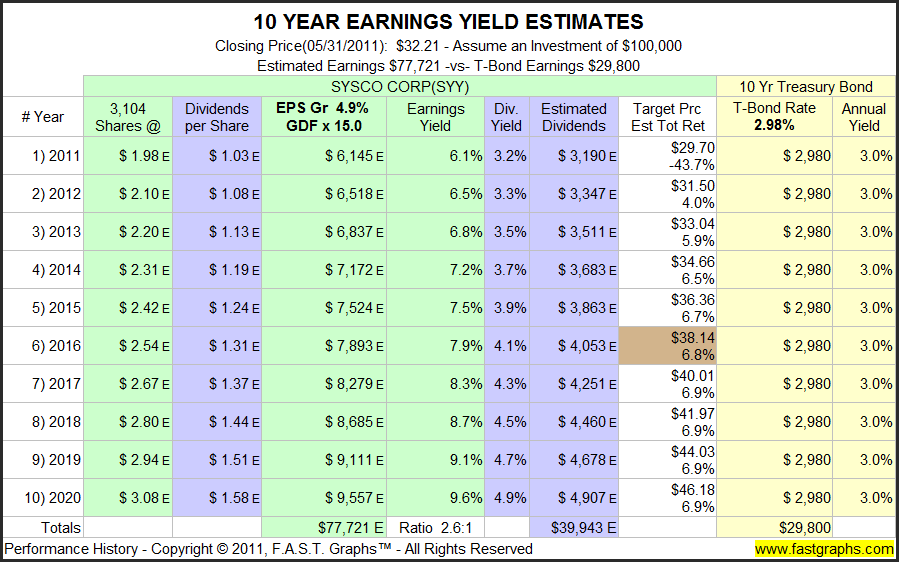

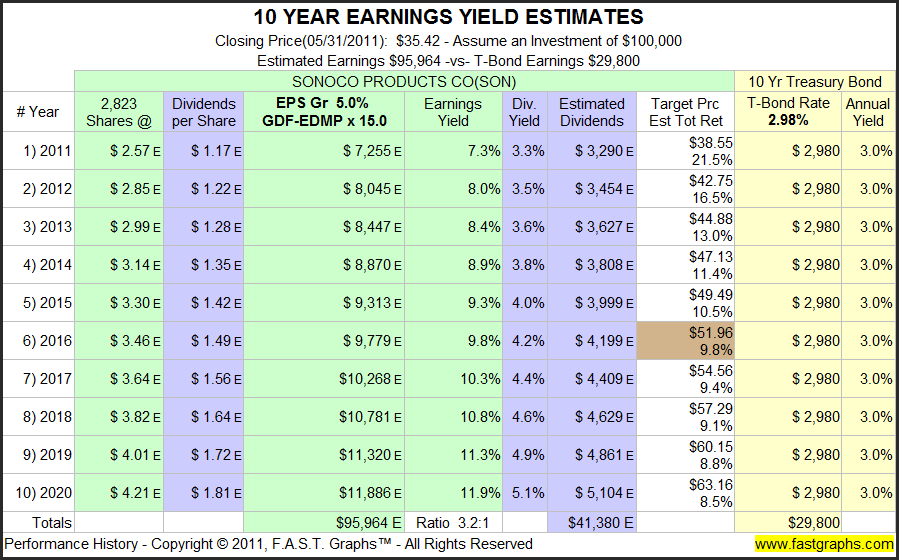

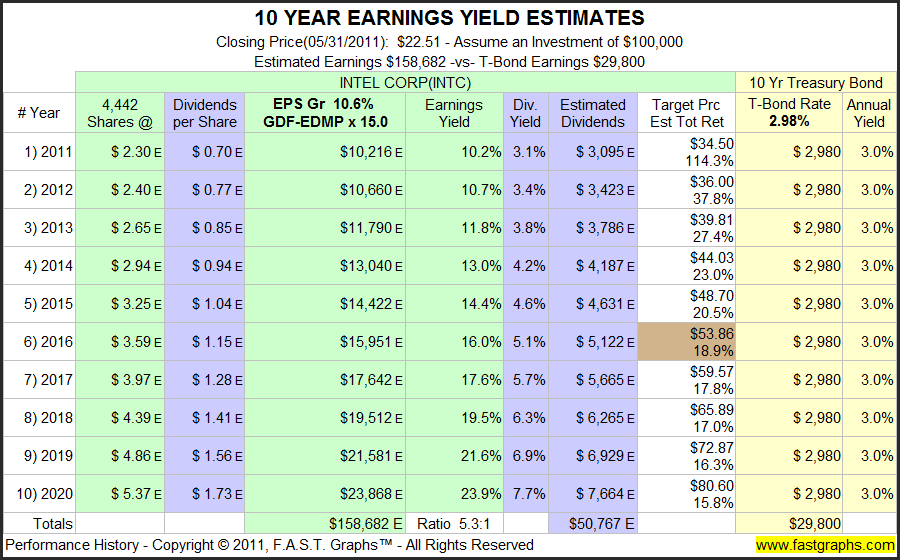

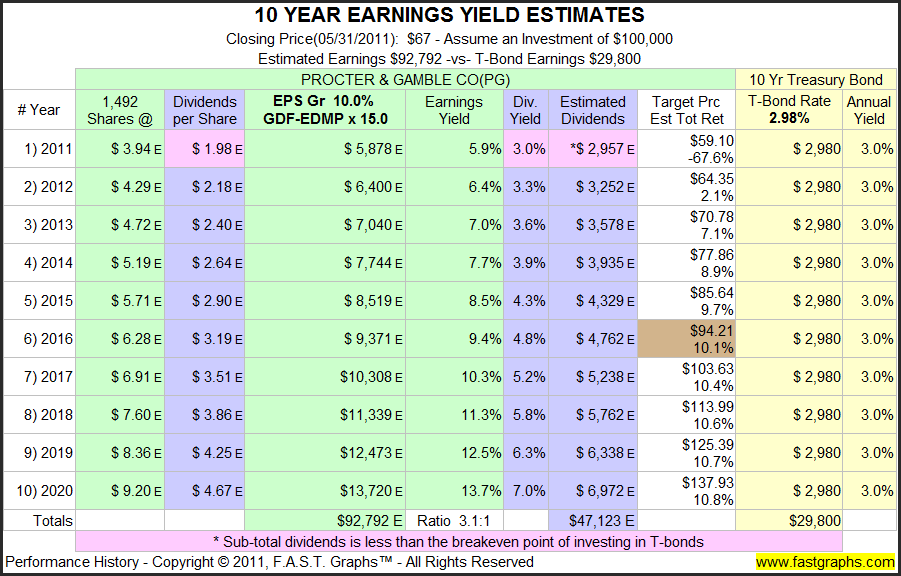

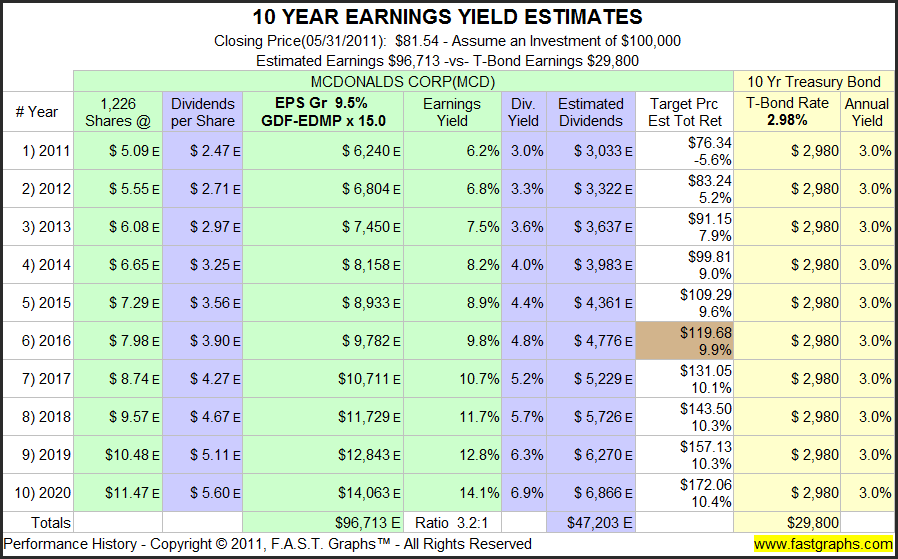

Ten-year Earnings Yield and Dividend Estimator

The following F.A.S.T. Graphs™ 10-year earnings yield estimators are calculated based on consensus of leading analysts’ forecast five-year earnings growth rates on each company. The additional five years is simply an extrapolation that is calculated in order to provide a comparison to a 10-year Treasury Bond. Consequently, the reader should understand that these calculations are hypothetical, but hopefully at least reasonable in nature.

They are offered to provide a depiction of the possible rewards of owning dividend growth stocks versus bonds in today's low interest rate environment. Readers should also keep in mind that under normal circumstances bonds would be offering yields higher than the dividend rates on these companies. These higher than normal yields indicate attractive stock price valuations. Therefore, the unusual income opportunity that dividend growth stocks are providing should not go unnoticed.

Here are a few comments to assist the reader with interpreting the graphs. For purposes of this article the focus should be on the blue columns which deal with dividends. When the columns associated with dividends on these graphs are blue, it indicates yields greater than the 10-year Treasury Bond comparison (yellow columns). The key takeaway is the potential greater total income stream that the dividend growth stocks may provide. Of course the reader should also keep in mind that there is no guarantee that the dividend levels depicted will be achieved. On the other hand, the 10-year Treasury Bond interest payments are the guaranteed rate.

Altria Group, Inc. (MO)

(Click to enlarge)

AT&T Inc. (T)

(Click to enlarge)

Duke Energy Corp. (DUK)

(Click to enlarge)

Dominion Resources Inc. (D)

(Click to enlarge)

Kimberly-Clark Corp. (KMB)

(Click to enlarge)

Philip Morris International (PM)

(Click to enlarge)

RPM International Inc. (RPM)

(Click to enlarge)

Unilever PLC-ADR (UL)

(Click to enlarge)

Waste Management Inc. (WM)

(Click to enlarge)

(Click to enlarge)

Campbell Soup Co. (CPB)

(Click to enlarge)

Kraft Foods Inc. (KFT)

(Click to enlarge)

Novartis AG-ADR (NVS)

(Click to enlarge)

Genuine Parts Co. (GPC)

(Click to enlarge)

Sysco Corp. (SYY)

(Click to enlarge)

Sonoco Products Co. (SON)

(Click to enlarge)

Intel Corp. (INTC)

(Click to enlarge)

Clorox Co/DE (CLX)

(Click to enlarge)

Procter & Gamble Co. (PG)

(Click to enlarge)

McDonalds Corp. (MCD)

(Click to enlarge)

Summary and Conclusions

Hopefully this two-part series has crystallized the extraordinary and unusual nature of today's interest rate environment in the minds of the reader. As the saying goes, "extraordinary times require extraordinary measures." Under a more normal environment we would not take such an onerous view towards bonds. Fixed income investments have long held a proper and rightful place in the portfolios of prudent investors.

The principles of proper diversification are valid and necessary when dealing with uncertain markets. On the other hand, to mindlessly invest in a dangerous and obvious asset class for the sole sake of diversification does not make sense to us. We believe that investors should always think their way through the process of allocating their assets and building their portfolios.

One of the best ways to accomplish this is to simply run the numbers out to their logical conclusions. When this process is done with bonds today, their validity as an asset choice is at the very best questionable. Consequently, given the requirement to choose an asset allocation between stocks, bonds and cash; today we choose stocks and cash. In lieu of bonds, we are replacing that asset class with blue-chip dividend growth stocks. In the future, if and when interest rates normalize, we would reconsider a bond allocation.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Disclosure: I am long MO, KMB, PM, UL, HNZ, CPB, KFT, NVS, GPC, SYY, INTC, CLX, PG, MCD.

No comments:

Post a Comment